Wedding planner insurance

Wedding planner insurance

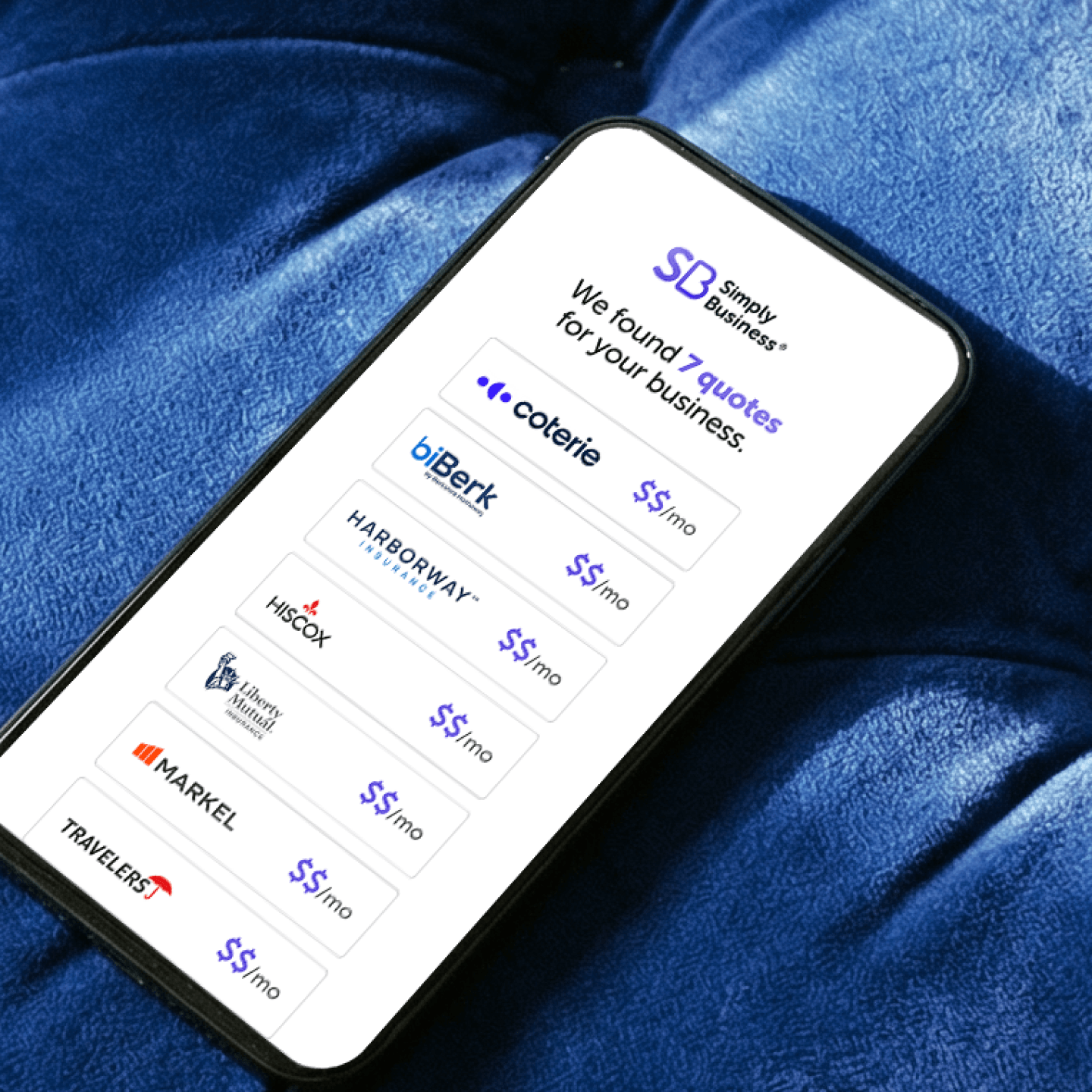

One application, multiple quotes.

All in one place.

Essential Coverage

From

$16.75

/month*

Could help cover claims against your business for property damage and injuries to others.

What’s included:

General Liability

Coverage limits: $100K to $2M†

Get multiple quotes in less than 10 mins

Essential Coverage

From

$16.75

/month*

Could help cover claims against your business for property damage and injuries to others.

What’s included:

General Liability

Coverage limits: $100K to $2M†

Get multiple quotes in less than 10 mins

Would you rather pick and choose your coverage? Explore all options

Over 1 million customers worldwide.

Buy instantly online.

Written by

Wedding Planner Insurance You Can Say “I Do” To

You help couples make memories that will last a lifetime. A wedding day is, as they say, the first day of the rest of someone’s life. While they’re making memories, who’s thinking about your business’s future?

That’s where wedding planner insurance comes in.

At Simply Business, we offer wedding planner business insurance policies that can cover your job’s specific financial risks.

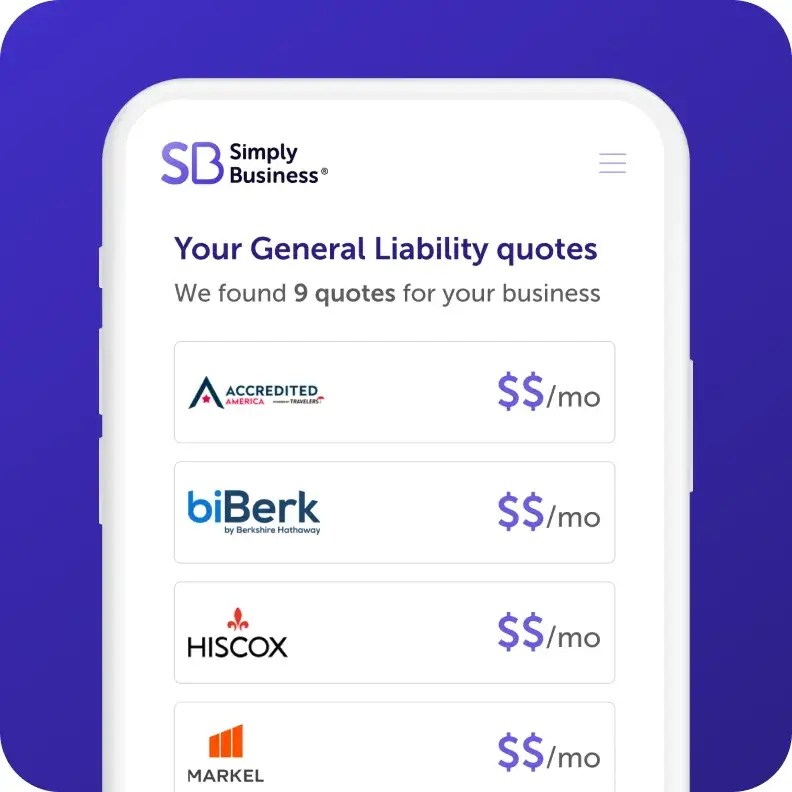

First, answer some questions about your business. Then we’ll show you coverage that fits your needs. After you compare quotes, choose the option that works best for your wedding planning business.

The best part? It takes less than 10 minutes. That’s less time than most reception speeches!

Ready to get hitched to the right policy? Let’s get you covered.

What Type of Wedding Planner Insurance Do I Need?

General Liability

A foundational insurance coverage to help handle costs from third-party accidents, property damage, and bodily injury.

From

$16.75

/month*

Workers’ Comp

Coverage to help take care of employees who get sick or injured on the job. Most states require this coverage for small businesses with full- or part-time employees. It also can benefit business owners who don’t have employees.

From

$38.91

/mon*

From

$25.83

/month*

Business Insurance Policies Available for Wedding Planners:

- General liability insurance

- Workers compensation insurance

Benefits:

- It can protect your business from certain claims.

- It can cover damages caused by your negligence.

- Proof of insurance can help clients feel good about your work.

- It may be required where you’re located.

Business insurance —

a quick explainer

Learn more about policies for small businesses, what they cover, why you might need them, and how we can help – all in just 60 seconds.

What Types of Wedding Planner Business Insurance Do I Need?

Wedding coordinator insurance coverage is a bundle of individual policies that can protect your business from financial risks. But different incidents can pose different risks to your business. That’s why we’ll review different types of business insurance and how they can help financially protect your business from those risks.

General Liability Insurance

General liability insurance is also known as commercial general liability insurance. It’s insurance coverage that can protect you from the financial risks resulting from third-party accidents, bodily injury, or property damage.

It’s your job as a wedding planner to make sure the day goes smoothly and is enjoyable for everyone. A lot of things had to go right for a couple to make the decision to get married, and unfortunately, there are a lot of things that could go wrong on the big day.

You can’t always predict things that are out of your control. And you’re not the only business owner facing financial risks. Business owners are commonly sued for several types of incidents. Consider slip and fall accidents. Those claims are common and pricey, costing an average of $20,000. According to The Knot, that’s about the average cost of a wedding these days.

Think about it: What would happen if tomorrow, a client sued you for $20,000? Where would that money come from? How would you pay for a lawyer to represent you?

It’s hard to think of a situation in the abstract, so let’s look at a specific scenario:

Malika created a once-in-a-lifetime experience for the wedding couple. She arranged for a contractor to set up an outdoor tent for the reception.

While entering the tent for the reception, the bride tripped and fell, spraining her ankle. She tripped over Malika’s laptop cord.

While their guests enjoy the reception, the newlyweds go to urgent care to get the bride’s ankle examined. After the event, they sue Malika for the cost of the bride’s medical bills, claiming that her carelessness led to the incident.

Without a general liability policy, Malika may need to pay the claim out-of-pocket. This could hit her business hard financially. If she hires a lawyer to defend her business, that will cost more money out-of-pocket.

With wedding planner insurance, Malika’s coverage could help pay the cost of the claim, medical costs, and lawyer fees, up to her policy’s limit.

General liability insurance typically covers third party:

- Bodily injury

- Third-party accidents

- Property damage

- And more

General liability insurance typically does not cover:

- Professional services

- Workers compensation or employee injury

- Commercial auto

- Damage to your work

- And more

Professional liability insurance

Professional liability insurance is a type of coverage that can financially protect your business from the results of incidents like negligence, libel or slander, copyright infringement, and more.

Your job is to make the happy couple feel special. It doesn’t feel great if your actions caused them harm in some way. But not all risks are as tangible as say, a sprained ankle from a fall.

Let’s look at a scenario of how a professional liability policy could come into play:

Malika plans another wedding with 150 people on the guest list. The caterers plan to have enough food to feed all 150 people.

Some guests RSVP last minute, saying they can’t make it. Malika received the emails but forgot to update the caterers of the change.This means that there was a ton of food left over, due to Malika’s error.

The newlyweds sue Malika for her negligence in not updating the caterers. They file a claim for the cost of the plates that weren’t cancelled.

Without professional liability coverage, Malika may have to pay the claim out-of-pocket, and if Malika’s wedding planner business doesn’t have any savings to rely on, it could put her in debt.

Malika could also be responsible for paying a lawyer to represent her business. And legal fees add up. They could even end up being more than the claim itself!

If Malika had professional liability coverage, the situation would likely be different. Instead of facing the claim and legal fees on her own, she’d have her policy to rely on. Her claim and the legal fees could be covered by her policy, up to its limit.

Workers Compensation Insurance

As a wedding planner, you often collaborate with several vendors and organizations to make your clients’ big day unforgettable. Eventually you may decide to hire an employee, either part-time, full-time, or just for a season.

In that case, you may need workers compensation insurance. Most states require this coverage, also referred to as workers comp. It helps protect your business financially if an employee gets sick or injured while working for you.

Creating your clients’ most memorable day is enough pressure on its own. Imagine having to worry about the well-being of your employees on top of that. The average claim for a workplace injury is $41,000. Workers comp coverage could save your business from financial ruin.

Workers compensation insurance typically covers:

- Death benefits

- Lost wages

- Rehabilitation costs

- Medical expenses

Why Get Wedding Planner Business Insurance

You may be the type of wedding planner who works as a day-of coordinator. Or maybe you handle the whole kit and kaboodle, from beginning to end.

If you’re so good at organization and following a checklist or plan, you should be able to avoid risk, right? Why bother getting wedding planner business insurance?

Making a mistake or experiencing an accident could seem as rare as a couple landing their first choice venue on the exact date they desire. But in reality, it’s a lot more common. In fact, a report estimated that 36%-53% of businesses surveyed get involved in a lawsuit each year.

If your wedding planning business gets involved in a lawsuit, you could be facing a hefty bill. These are some of the more common claims. Let’s take a look at what they cost:

- $50,000 for reputational harm (such as libel or slander)

- $20,000 for a customer slip and fall

- $30,000 for customer injury or damage

Any of these claims could mean financial ruin. Knowing you’re covered up to your policy’s limit can put your mind at ease.

Luckily, getting wedding coordinator insurance is easy. Answer some questions about the ins-and-outs of your business. Then Simply Business can help you compare coverage options using our free quote comparison tool here.

The good news is that business insurance is typically affordable and it takes less than 10 minutes to get a quote — less time than it takes to arrange a wedding reception centerpiece!

What Does Wedding Planner Insurance Cost

Try our insurance calculator.

Get a quick estimate in just 3 steps.

Wedding Coordinator Insurance FAQs

Why Wedding Planners Choose Simply Business

Small business insurance is what we do. Whether it’s covering you for accidents and errors, meeting workers’ comp requirements, or financially protecting your business from the unexpected, we can help find the coverage you need for your business.

Start your quote

Answer a few questions about

your business in one form.

Review quotes

Compare quotes side by side from top-rated insurers and customize your coverage.

Get protected in minutes

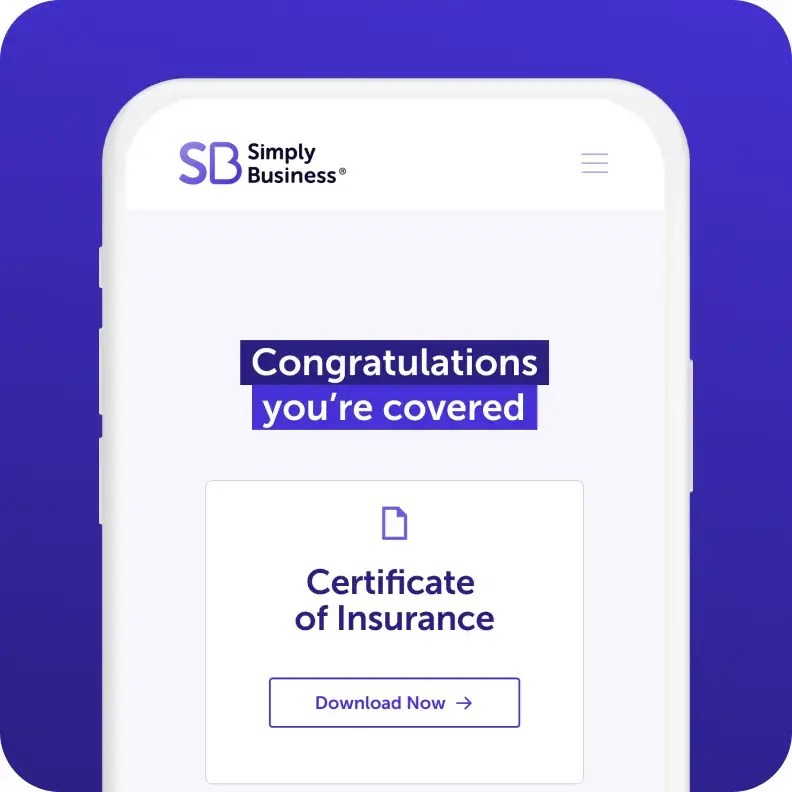

Choose your policy, and get instant proof of insurance – all online, and all within 10 minutes.

Written by

Our +1 million customers are big fans. And you will be too.

I went online, looked around, and found Simply Business. The process was so seamless. I got my certificate within minutes. It was just phenomenal.

Karen

Owner of Tangaza Bath & Body Studio LLC

With Simply Business I know I can look at different carriers, but also see all my stuff in the same place… a lot of [insurance] providers don’t offer a variety of coverage, all in one place.

Jef

Owner of Bunker83 LLC

It wasn’t overwhelming to figure out what was covered and what wasn’t covered. And the cost was competitive.

Kim

Owner of Room to Breathe Professional Organizing

Feel confident in your choice.

We partner with a range of top-rated carriers and use smart technology to match you with policies that fit your specific business, your risks, and budget.

400+

business types covered

1M+

customers worldwide

18

top-rated carriers

We’ve Got More Helpful Information

9-minute read

A General Liability Insurance Guide for Small Business

8-minute read

Busy Wedding Season: Readiness Checklist

*The displayed price for each product is a monthly estimate calculated from the 10th percentile of relevant policies sold by Simply Business (e.g., General Liability data is used for General Liability estimates). This estimate uses data from relevant policy sales between July–December 2025. Final price and payment terms, which may include an initial down payment, are subject to change based on your state, selected insurance provider, and specific business details.

† Limits may vary by state and nature of your business.