Small Business Insurance Coverage Options

Customized coverage for LLCs, freelancers, and small businesses.

General

Liability

From $20.75/month*

Business

Owner’s Policy

From $33.75/month*

Workers’ Compensation

From $38.91/month*

Professional Liability

From $25.83/month*

Additional Coverages

More options to protect your business property, employees, and equipment.

Trustpilot | 4.1 rating

Trusted by more than 1 million small business owners worldwide.

Google | 4.4 rating

General liability insuranceFrom $20.75/month*

Workers’ comp insuranceFrom $38.91/month*

Professional liability insuranceFrom $25.83/month*

Business owner’s policy insurance (BOP)From $33.75/month*

Additional CoveragesMore options to protect your business property, employees, and equipment.

Trustpilot | 4.1 rating

Trusted by more than 1 million small business owners worldwide.

Google | 4.4 rating

What is Business Insurance?

Business insurance generally includes several types of policies designed to protect your business from financial losses due to accidents, lawsuits, property damage, and more.

How much is small business insurance?

The cost of small business insurance varies by industry and is determined by a number of factors including business size, industry, location, and claims history.

From

$20.75

/month*

What does small business insurance cover?

Small business insurance can help cover:

- Stolen or damaged gear

- Third-party accidents, property damage, and bodily injuries

- Claims of negligence or mistakes in your work

- Medical bills and lost wages

Who needs small business insurance?

Any business, regardless of size or industry, can benefit from commercial insurance.

We recommend it for business owners, whether you’re a sole proprietor, LLC, work with a partner, or manage a small team.

Access to top carriers:

Types of Business Insurance Coverage

Business insurance usually refers to one or more coverages suited to your type of small business. Here are the foundational insurance policies we most often recommend, and how they can help protect your small business:

General Liability

If you interact with clients in any way, we typically recommend having a general liability insurance policy. This foundational insurance coverage can help you handle costs from third-party accidents, property damage, legal expenses, and bodily injury.

From

$20.75

/month*

Business Owner’s Policy (BOP)

A practical way to get comprehensive and affordable coverage without juggling multiple policies is with a business owner’s policy (BOP). It bundles three key coverages — general liability, commercial property, and business interruption insurance — into one convenient package.

From

$33.75

/month*

Professional Liability

This coverage is crucial for protecting you from claims of negligence or mistakes in your work. If a client is unhappy with your service and sues you for financial loss, this policy helps cover your legal defense and potential settlements.

From

$25.83

/month*

Workers’ Compensation

If you have employees — even just one apprentice — most states require you to carry workers’ compensation. This policy covers medical bills and lost wages for employees who get injured or become ill on the job.

From

$38.91

/month*

Additional Coverages

The following coverage options act as specialized “add-ons” that fill specific gaps the foundational insurance policies don’t cover—such as protecting equipment in transit (Inland Marine), covering your inventory (BPP), or shielding you from professional mistakes (E&O).

Business Personal Property

Business personal property (BPP) insurance typically covers the equipment, furniture, fixtures, and inventory that you own, use, or rent inside your workspace.

Inland Marine Insurance

This coverage can financially protect equipment and inventory that’s in transport or stored offsite.

Errors & Omissions

An E&O policy typically covers the costs of legal claims or damage caused by errors or unintentional omissions from your work.

Who Needs Small Business Insurance?

Any business that provides professional services, offers a skilled trade, handles customer data, or owns physical business assets should carry small business insurance to protect against lawsuits and financial loss. Essentially, any business that interacts with customers, owns property, or employs staff should consider small business insurance. Here are some examples of small businesses and why they need insurance:

Handyperson

Why You Need It:

Whether you’re a solo fix-it pro or managing a small crew, a single slip of a drill or a stolen toolbox can disrupt your entire schedule. Handyman insurance is designed to protect your specialized tools, your business, and your team, ensuring that a minor accident on a service call doesn’t derail your hard-earned reputation.

Housekeeping

Why You Need It:

From fresh linens to sparkling bathrooms, your work can transform a home. But even the most careful housekeeper can have an off day — a scratched floor, a product spill, or a pulled muscle after hauling supplies. Housekeepers insurance can help protect your business, tools, and team, so one mishap doesn’t make a mess.

Painters

Why You Need It:

As a painter, careful preparation is key to delivering flawless results and avoiding costly errors. Painters insurance works the same way for your business — helping protect you from accidents, property damage, theft, or injuries on the job.

E-commerce & online retailers

Why You Need It:

When you run an online shop, your work may be primarily virtual, but the risks your small business faces are all-too real. Among them are product liability, copyright infringement, data breaches, and ransomware.E-commerce and online retailers insurance acts as a digital and physical safety net.

Lawn care services

Why You Need It:

As a lawn care pro, you can turn scorched turf into a lush green carpet. But accidents are like weeds — they can take root no matter how much you prepare. And having the right insurance policies can help protect your lawn care business when the inevitable mishaps crop up.

Craft vendor

Why You Need It:

Whether you’re pouring candles for a holiday market or showcasing jewelry at an art fair, a lot can go sideways between setup and teardown. And when the unexpected happens, like a customer tripping over your display or a tent pole collapsing in a crowded aisle, craft vendor insurance helps ensure one bad day doesn’t shut down the business you’ve built by hand.

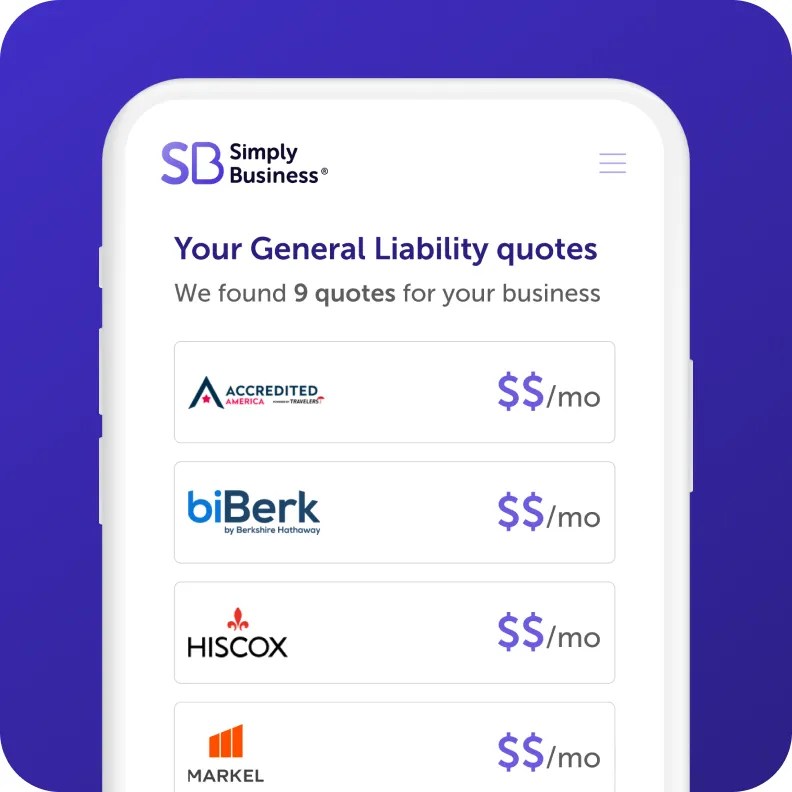

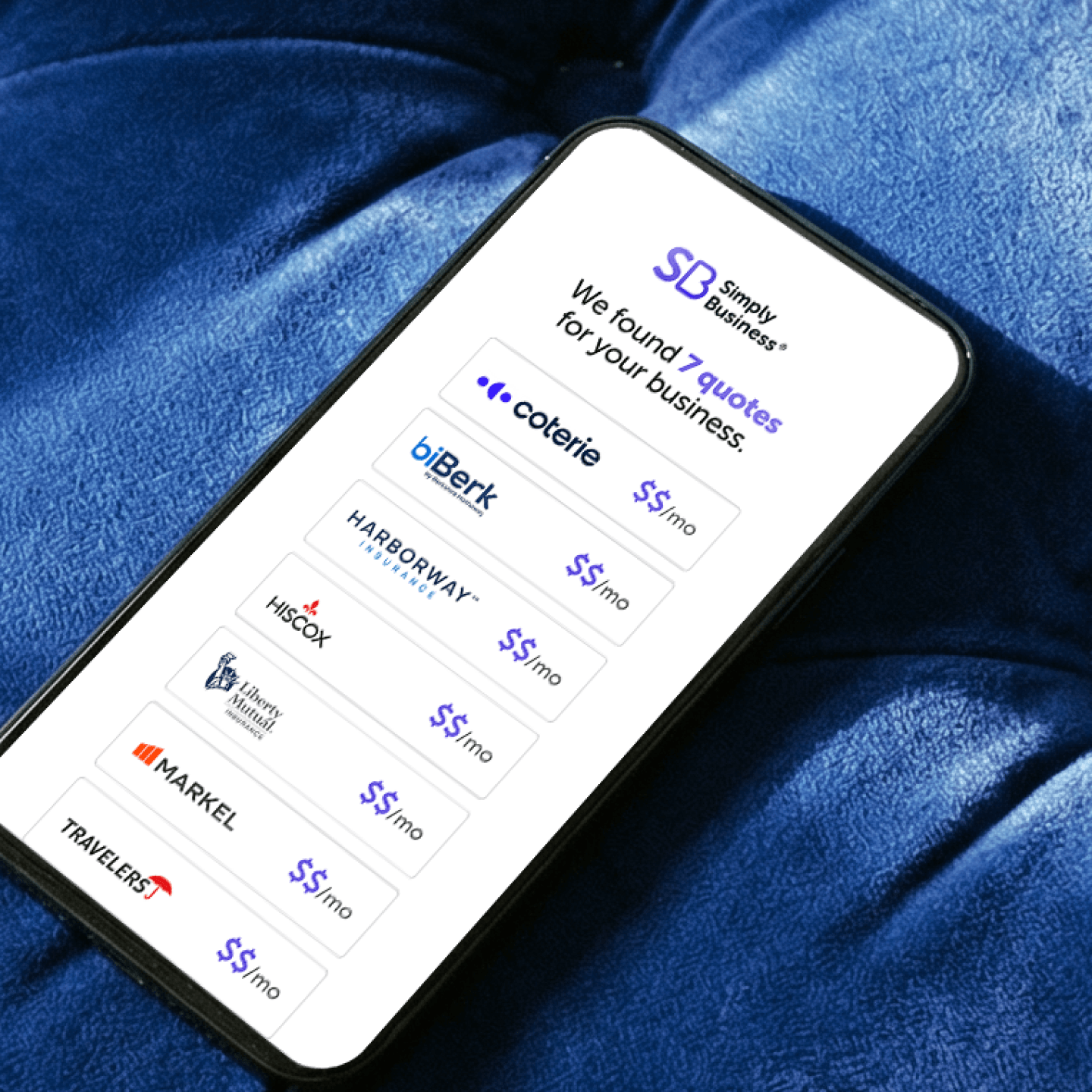

How to Get Small Business Insurance Online

Step 1: Start your quote

Answer a few questions about

your business in one form.

Step 2: Review quotes

Compare quotes side by side

from top-rated insurers and customize

your coverage.

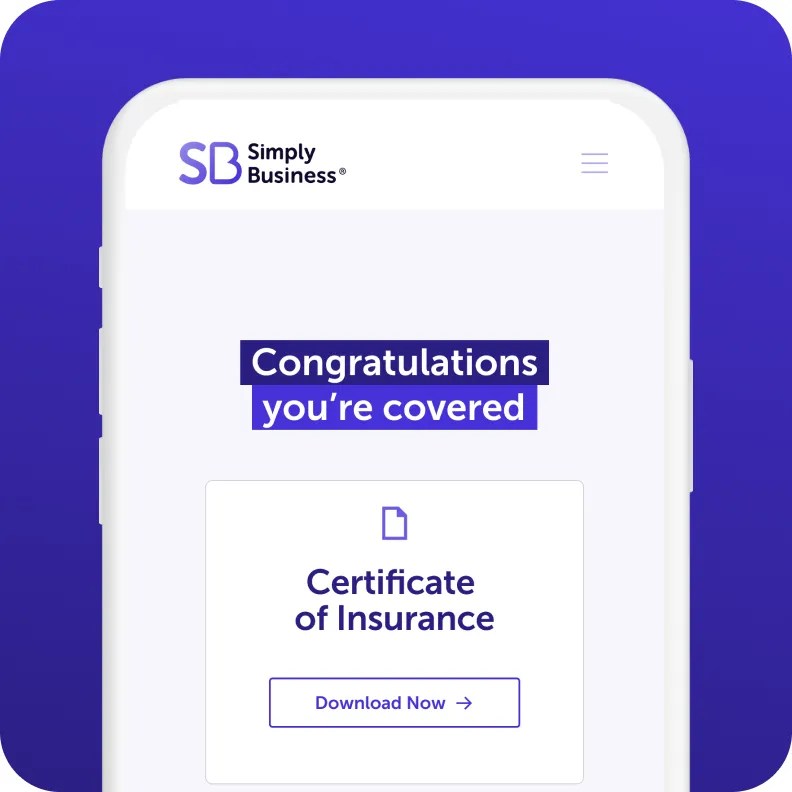

Step 3: Get protected in minutes

Choose your policy, and get

instant proof of insurance – all online,

and all within 10 minutes.

How Much Does Business Insurance Cost?

The cost of business insurance varies across industries. There are also several factors that affect your premium, including:

- Business size

- Industry

- Location

- Claims history

- Policy limits

Here’s a look at the median prices1 our customers pay for our most common policy types.

Insurance Policy

Median Monthly Cost

Median Annual Cost

General Liability

$42

$504

Business Owner’s Policy

$48

$576

Professional Liability

$42

$504

Workers’ Compensation

$101

$1,212

1Data from Simply Business customers who purchased at least one or a combination of general liability, business owner’s policy, professional liability, or workers’ compensation policies from July 1, 2025 to December 31, 2025.

Insurance Policy

Median Monthly Cost

Median Annual Cost

General Liability

$42

$504

Business Owner’s Policy

$48

$576

Professional Liability

$42

$504

Workers’ Compensation

$101

$1,212

1Data from Simply Business customers who purchased at least one or a combination of general liability, business owner’s policy, professional liability, or workers’ compensation policies from July 1, 2025 to December 31, 2025.

Why Compare Business Insurance With Simply Business?

Simply Business helps small businesses compare quotes and buy insurance from leading carriers in minutes. We offer a wide range of options, ensuring you find the coverage that best fits your needs.

With most policies, you can receive your COI instantly, proving your coverage and meeting contractual requirements.

Business Insurance FAQs

Is business insurance a legal requirement?

Laws vary by state, but it’s common for general liability insurance to be required for small business owners. Your free quote takes your location into account, and our licensed agents can help you determine your needs. If you have employees, you’ll need to have workers’ compensation coverage.

Can I change my policy after I buy it?

Yes, you can usually modify your coverage as your business needs change. If you have questions about updating, renewing, canceling or changing your policy, you can find information in your online account. Or you can call one of our licensed insurance experts for help at 855-869-5183.

How long does it take to get a Certificate of Insurance?

You can get access to your certificate of insurance in minutes through your online account. Request a copy via email or download a digital COI instantly.

What does General Liability actually protect me from?

General liability (GL) insurance covers the costs of claims, medical bills, legal expenses, and more for your small business. It also helps cover your employee or employees if they cause the damage. Some of the things it typically covers include:

- Faulty products

- Third-party property damage

- Third-party injuries

- Advertising injury

Is my business insurance tax deductible?

Yes, you can typically deduct insurance premiums when filing their business income taxes. We strongly recommend talking to an accountant for more information about your state’s tax laws, though.

Do I need insurance if I work from home?

We recommend you have home-based business insurance. It’s a type of coverage that can typically help cover the costs of an unexpected accident, injury, or property damage. It’s designed to help cover your business if it’s primarily located within your home.

Because most traditional homeowners policies don’t cover incidents relating to a home business, it’s important to get additional coverage.

How do I file a business insurance claim?

Insurance claims are handled by your insurance carrier. Please contact them for the appropriate next steps. You can find a list of carriers and more information on our Insurance Claims page.

What are some other situations that require business insurance?

Even when it’s not required by law, business insurance may be required for other business needs and operations, such as;

- Applying for licenses. Many regulatory, governmental, and other bodies require an active insurance policy to grant a license.

- Signing a lease. Your landlord may require you to have general liability insurance and commercial property insurance.

- Competing for contracts. Clients may require you to have professional liability insurance.

State Guides for Insurance

Find out what’s required in the state or states where you operate:

Our +1 million customers are big fans. And you will be too.

I went online, looked around, and found Simply Business. The process was so seamless. I got my certificate within minutes. It was just phenomenal.

Karen

Owner of Tangaza Bath & Body Studio LLC

With Simply Business I know I can look at different carriers, but also see all my stuff in the same place… a lot of [insurance] providers don’t offer a variety of coverage, all in one place.

Jef

Owner of Bunker83 LLC

It wasn’t overwhelming to figure out what was covered and what wasn’t covered. And the cost was competitive.

Kim

Owner of Room to Breathe Professional Organizing

*The displayed price for each product is a monthly estimate calculated from the 10th percentile of relevant policies sold by Simply Business (e.g., General Liability data is used for General Liability estimates). This estimate uses data from relevant policy sales between July–December 2025. Final price and payment terms, which may include an initial down payment, are subject to change based on your state, selected insurance provider, and specific business details.

Page last updated: