Small Business Insurance in North Carolina

Get a price estimate in just three steps

Rates as low as $20.75/month*

Get a price estimate in just three steps

Rates as low as $20.75/month*

Over 1 million customers worldwide.

Buy instantly online.

Written by

North Carolina Business Insurance

With low business costs, a supportive regulatory climate, and a skilled workforce, North Carolina (NC) offers many advantages to new business owners.

The state’s business landscape stretches from Charlotte’s financial corridor to the tech hubs around the Research Triangle Park, and the hospitality and trade markets in the western mountains. Each industry carries different risks, and insurance requirements can vary, based on your workforce, where you operate, and the contracts you sign.

Knowing what business insurance in North Carolina applies to you can help protect your business and keep you compliant as you grow.

On this page

Find the information you need quickly

Is Business Insurance Required in North Carolina?

At the state level, businesses may be required to carry workers’ compensation coverage for employees and commercial auto insurance in NC for vehicles used in their operations, though specific requirements depend on your workforce and the vehicles your business operates. There also may be additional requirements in the county, city, or town where you operate. You should check with local insurance and legal professionals who can help you determine which coverages you need and at what limits.

General liability and professional liability aren’t required by the state, but commercial landlords and client contracts may require proof of coverage before you can sign a lease or start work.

What Types of Small Business Insurance Are Required in North Carolina?

North Carolina’s insurance requirements depend on your industry, the number of people you employ, and where you operate. Here’s how the most common policies break down.

Workers’ Compensation Insurance in North Carolina

Workers’ comp insurance can help cover medical bills, lost wages, and rehabilitation costs if an employee suffers a work-related injury or illness.

In North Carolina, workers’ compensation is required for most businesses with three or more employees. For corporations, all officers count toward this total. For LLCs, members are generally excluded from the count unless they specifically elect to be covered.Some exemptions apply, including domestic servants and farm laborers with fewer than 10 full-time, non-seasonal workers.

Even if you have fewer than three employees, workers’ comp can still benefit solo business owners or those with one or two employees. Plus, some contracts and clients may require it, and this coverage can help protect you from paying out of pocket if an on-the-job injury occurs.

Professional Liability Insurance (E&O) in North Carolina

Professional liability insurance, also known as Errors and Omissions (E&O) insurance, is often recommended for businesses that provide advice and guidance to clients. Professional liability can help cover claims of negligence, errors that result in unsatisfactory finished work, and legal defense costs.

While not required by state law, professional liability insurance in NC is often a common contractual or firm requirement for consultants and those in certain fields, such as legal services and real estate.

General Liability Insurance in North Carolina

General liability insurance in North Carolina isn’t mandated as state law, but many commercial leases in cities such as Charlotte or Raleigh often require it. It also may be something required by contractors, clients, or professional firms.

General liability is a foundational coverage that helps protect against risks North Carolina businesses often face, including third-party bodily injury, property damage, and personal and advertising injury.

Business Owner’s Policy in North Carolina

A Business Owner’s Policy (BOP) is essentially the “bundled deal” of the insurance world. In North Carolina, it is a popular choice for small businesses (like retail shops, restaurants, or professional offices) because it combines general liability and commercial property coverage into one policy, often at a lower premium than buying them separately.

Here are the specific things a BOP typically covers for a North Carolina business owner:

1. General Liability (GL)

This protects you if your business is legally responsible for causing harm to someone else or their stuff.

- Customer Injuries: If a client slips on a rainy floor at your shop in Raleigh and breaks their arm, the BOP helps pay for their medical bills.

2. Business Personal Property (BPP)

BPP insurance protects your equipment, furniture, inventory, and more. It can help with the cost to replace all those important items in the event they’re stolen, damaged, or destroyed.

A business personal property policy can cover financial claims involving:

- Theft of business property

- Damage to the business property

- Loss of business property

- And more

Commercial Auto Insurance in North Carolina

If your business owns or operates vehicles, your personal auto policy may not cover accidents that happen during business use. A separate commercial auto policy can make a difference if you’re driving to jobsites, making deliveries, or transporting equipment.

In NC, commercial auto insurance is needed for all business-owned vehicles. North Carolina’s minimum liability limits (updated July 1, 2025) are $50,000 per person for bodily injury, $100,000 per accident for bodily injury, and $50,000 for property damage.

While Simply Business didn’t offer commercial auto insurance at the time this article was published, our licensed insurance agents can help you find providers that do.

Get free North Carolina business insurance quotes in 10 minutes or less.

Simply Business provides customized coverage options from top-rated small business insurers — all in just 10 minutes. We do all the leg work so you can sit back, compare quotes, and save.

How Much Does Business Insurance Cost in North Carolina?

Here are median monthly ranges for North Carolina business insurance costs:

Median Monthly Costs1

| General liability | $42 |

| Professional liability: | $33 |

| Workers’ compensation: | $117 |

| Business owner’s policy in North Carolina | $48 |

1Data from Simply Business customers located in NC, who purchased at least one or a combination of BOP, general liability, professional liability, and workers’ compensation policies from July 1, 2025 to December 31, 2025. The median costs shown are for illustrative purposes only; actual premiums vary by state, coverage limits, and individual business risk.

The cost of small business insurance in North Carolina depends on several factors, and pricing can vary significantly from one business to the next.

Some factors that affect your premium include:

- Payroll: Workers’ compensation premiums are tied to your payroll size and headcount. More employees and higher payroll can mean more exposure to risk and therefore higher premiums.

- Location: Premiums can vary depending on whether you operate in a metro area such as Charlotte or a smaller city in the western part of the state.

- Claims history: If claims have been filed against your policies in the past, you may see a higher rate at renewal time.

Who Needs North Carolina Small Business Insurance?

State-Specific Risks for Businesses in North Carolina

North Carolina businesses face risks that vary depending on where in the state you operate and your industry; the right insurance coverage can help protect against them.

Hurricane & Coastal Flooding

Businesses in Wilmington, the Outer Banks, and along the coast often face high exposure to hurricanes and flooding. Standard commercial property insurance typically does not cover flood damage, and in some coastal areas, windstorm and hail coverage also may be excluded from your policy. Businesses often need these protections in addition to their primary property policy.Business owners in these areas may need a separate flood insurance policy through the National Flood Insurance Program or a specialized windstorm endorsement through the NC Insurance Underwriting Association (NCIUA).

Adverse Weather and Employment Policies

North Carolina employers must consider how adverse weather impacts both their insurance and their business operations. There is no state-wide policy requiring that employers have an adverse weather policy. Therefore, employers have broad discretion over how they handle staffing during severe weather events. It’s important for North Carolina business owners to know that if they have an adverse weather policy, they must adhere to it.

Rapid Growth Risks

The tech and manufacturing boom in the Research Triangle Park has made the region among the fastest-growing tech hubs in the country. That growth increases exposure to professional liability and cyber-related claims, especially for startups handling sensitive client data or providing consulting services.The North Carolina Department of Insurance lists cyber liability insurance as an emerging coverage area for business owners.

Best North Carolina Business Insurance for Your Industry

Every industry has its own risk profile, and North Carolina business insurance requirements can affect the type and amount of coverage you may need for your industry.

Construction & Skilled Trades

North Carolina doesn’t require a surety bond or insurance as a condition to receive a general contractor’s license, but individual projects and building permits often do. While a surety bond isn’t a “universal” requirement for all, it is a mandatory alternative for those not meeting specific net worth or working capital thresholds set by the NC Licensing Board for General Contractors.

For commercial and public projects in Charlotte and other high-growth metro areas, owners and agencies may ask for higher commercial general liability limits (for example, at least $1 million per occurrence) as a condition of bidding or being awarded work.

Workers’ comp applies once you cross the state employee threshold.

Restaurants & Hospitality

Restaurants and bars that serve alcohol in North Carolina need a permit from the NC Alcoholic Beverage Control Commission. Liquor liability insurance can help protect your business if a customer causes harm after being served.

Liquor liability coverage may be included in your policy, depending on your carrier, whether you hold an active alcohol license, and the state where you operate.

Coastal restaurants and establishments also face the risk of power outages from storms. As an add-on to your BOP insurance, food spoilage coverage can help offset covered losses if refrigerated inventory is lost during an extended outage.

Tech & Professional Services

The Raleigh-Durham corridor and Research Triangle Park are home to a growing number of tech startups and consulting firms. North Carolina’s data breach notification law requires businesses to notify affected individuals and the Attorney General’s office if personal information is compromised.

Professional liability and cyber liability insurance can help cover the cost of those claims, including legal fees, notification requirements, and regulatory fines.

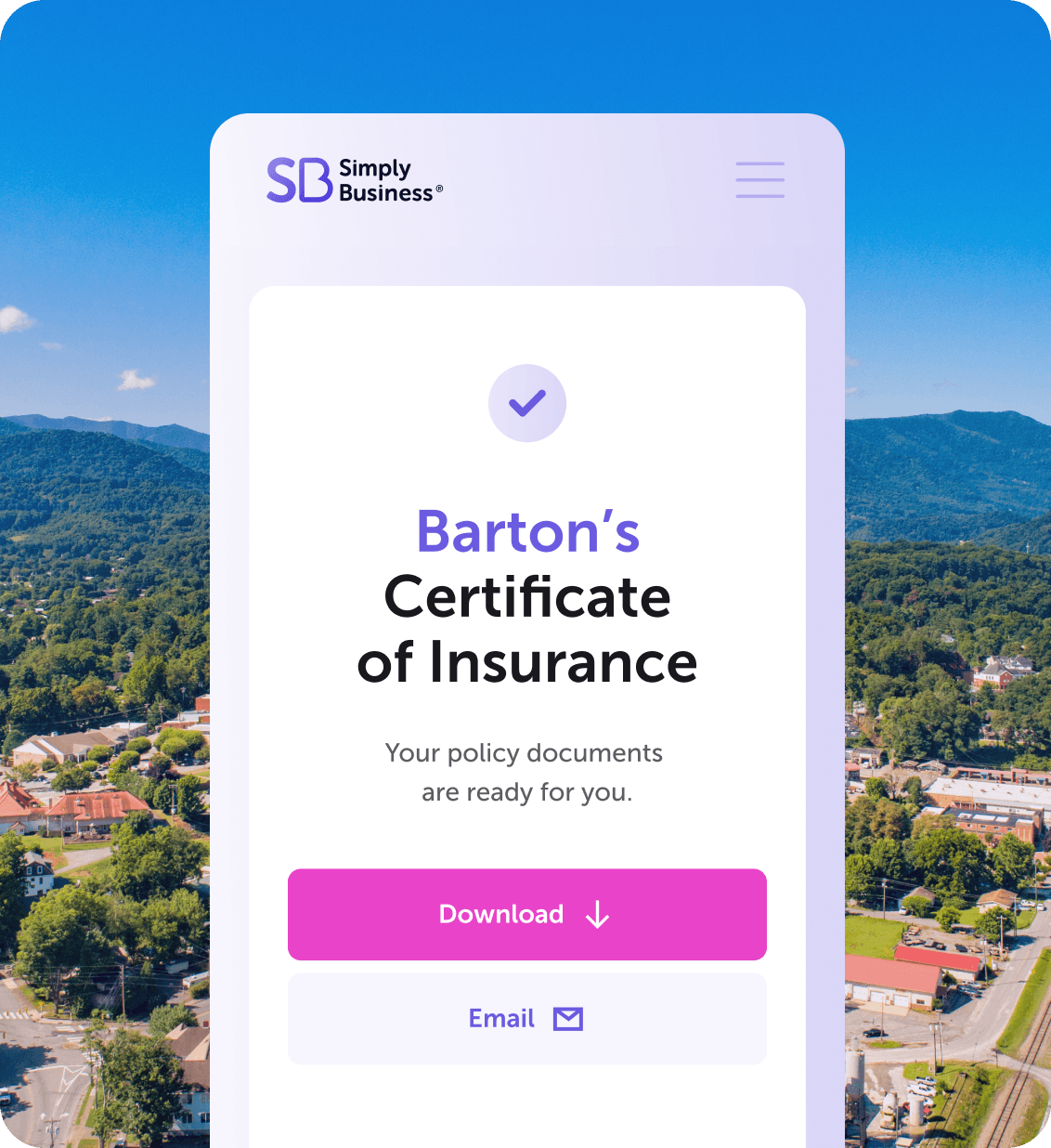

How to get a Certificate of Insurance in North Carolina

A Certificate of Insurance (COI) confirms your coverage is active and shows your policy limits. In North Carolina, you may need a COI before you can bid on contracts, sign a commercial lease, or get hired as a subcontractor.

With Simply Business you can request a COI directly through your online account when your policy is active. If you need to add an additional insured to your certificate, you can do that online as well.

FAQs About North Carolina Business Insurance

Do I need workers’ comp if I have only 2 employees?

North Carolina’s workers’ comp requirement kicks in at three or more employees. If you have two employees or less, you’re not required by state law to carry coverage.

However, some contractors or clients may still require it, and carrying a policy can protect you from paying out of pocket if an employee is injured on the job.

Is general liability required for an LLC in NC?

There is no state law that requires North Carolina LLC to carry general liability insurance. But many commercial landlords, clients, and some municipalities may require proof of GL coverage before signing a lease or awarding a contract.

Does a North Carolina general contractor need to cover subcontractors?

If you sublet work to a subcontractor without first confirming if they have workers’ compensation coverage, you can be held liable for their employees’ injuries under North Carolina law. And that applies even if the subcontractor has fewer than three employees.

Consider requesting a certificate of insurance from each subcontractor before work begins showing that they have their own workers’ compensation coverage.

What are the minimum commercial auto limits in NC?

North Carolina commercial insurance requires minimum liability limits of $50,000 per person for bodily injury, $100,000 per accident for bodily injury, and $50,000 for property damage for business-owned vehicles.

Our North Carolina customers are big fans. And you will be too.

The person I spoke with clearly explained my options and helped me understand what’s needed to protect my business. Her knowledge and level of customer support was off the charts.

Nina K.

Craft vendor, NC

Site was easy to follow. Covered what I needed. Cost was reasonable and quick process.

Tracie R.

Janitorial services, NC

The representative was wonderful. Super helpful, and ultimately helped me make the best decision.

Ryan S.

Restaurant, NC

Additional Information and State Resources for North Carolina Small Business Owners

North Carolina Department of Insurance

North Carolina Workers’ Compenestion State Requirements

North Carolina DMV: Commercial Auto Requirements

North Carolina Licensing Board for General Contractors

North Carolina General Permit Information

Written by