Business Owner’s Policy (BOP) for Small Businesses

General liability, property insurance, and more all in one convenient package. Get insuredfor as low as $33.75/month.*

Over 1 million customers worldwide.

Buy instantly online.

Written by

What Does a BOP Insurance Policy Cover?

A BOP is a package policy that typically bundles three types of small business insurance together:

General liability insurance

If business insurance were a house, general liability insurance could be the foundation. It can help cover costs from accidents caused by your business to third parties, as well as damage to someone else’s property.

A GL policy can also cover personal or advertising injury claims against your business, which can include claims of stolen ideas, invasion of privacy, libel, slander, and copyright infringement related to advertising.

Commercial property insurance

If you have a storefront, office space, or other building for your business, commercial property insurance can cover damages caused by fire, theft, weather, or other similar events. It can also cover damage to physical assets such as inventory, supplies, equipment, tools, and machinery.

Business interruption insurance

If your business is forced to close for a period of time (from a covered cause), business interruption coverage can help pay for lost income which can help get your small business back up and running sooner. This is also known as business income coverage.

Depending on your specific business, you can add optional coverage to your business owner’s policy to make it an even better fit. For example:

Cyber insurance

Employee theft coverage

Spoiled merchandise coverage

Forgery coverage

Equipment breakdown coverage

Simply Business gives you access to top insurance carriers.

Who Needs a Business Owner’s Policy?

Brick-and-mortar businesses with inventory and equipment, such as restaurants and retail stores, often can benefit from a BOP. A business owner’s policy could make sense for many small business owners who don’t have a lot of time to search for different coverages, prices, and providers.Brick-and-mortar businesses with inventory and equipment, such as restaurants and retail stores, often can benefit from a BOP. A business owner’s policy could make sense for many small business owners who don’t have a lot of time to search for different coverages, prices, and providers.

What Other Types of Insurance Do I Need?

Business insurance usually refers to one or more coverages suited to your type of small business. Here are the foundational insurance policies we most often recommend, and how they can help protect your small business:

General LiabilityFrom $20.75/month*

Workers’ CompFrom $38.91/month*

Professional LiabilityFrom $25.83/month*

Inland MarineFrom $20.83/month*

Business Personal PropertyFrom $25.83/month*

Errors & OmissionsFrom $33.75/month*

How Much is Business Owner’s Policy Insurance?

Compare prices from top carriers in under ten minutes.

What type of business do you want to insure?

What Some Customers are Paying for BOP2

California

Esthetician Services

- Corporation

- General liability coverage: Occurrence/aggregate limits: $1M/$2M

- Business personal property coverage: $40,000 limit/$500 deductible

- Quoted May 2026

$78

/month

Utah

Hair Salon

- Limited Liability Company (LLC)

- General liability coverage:

Occurrence/aggregate limits: $1M/$2M - Business personal property coverage: $20,000 limit/$500 deductible

- Quoted May 2026

$39

/month

Georgia

Restaurant

- Limited Liability Company (LLC)

- General liability coverage:

Occurrence/aggregate limits: $1M/$2M - Business personal property coverage: $60,000 limit/$500 deductible

- Quoted May 2026

$102

/month

2These examples are real insurance quotes generated on the dates above. They are for illustration purposes only. Your coverage options and pricing may differ based on the information you provide us about your particular business, the state you operate in, the number of employees, and other factors.

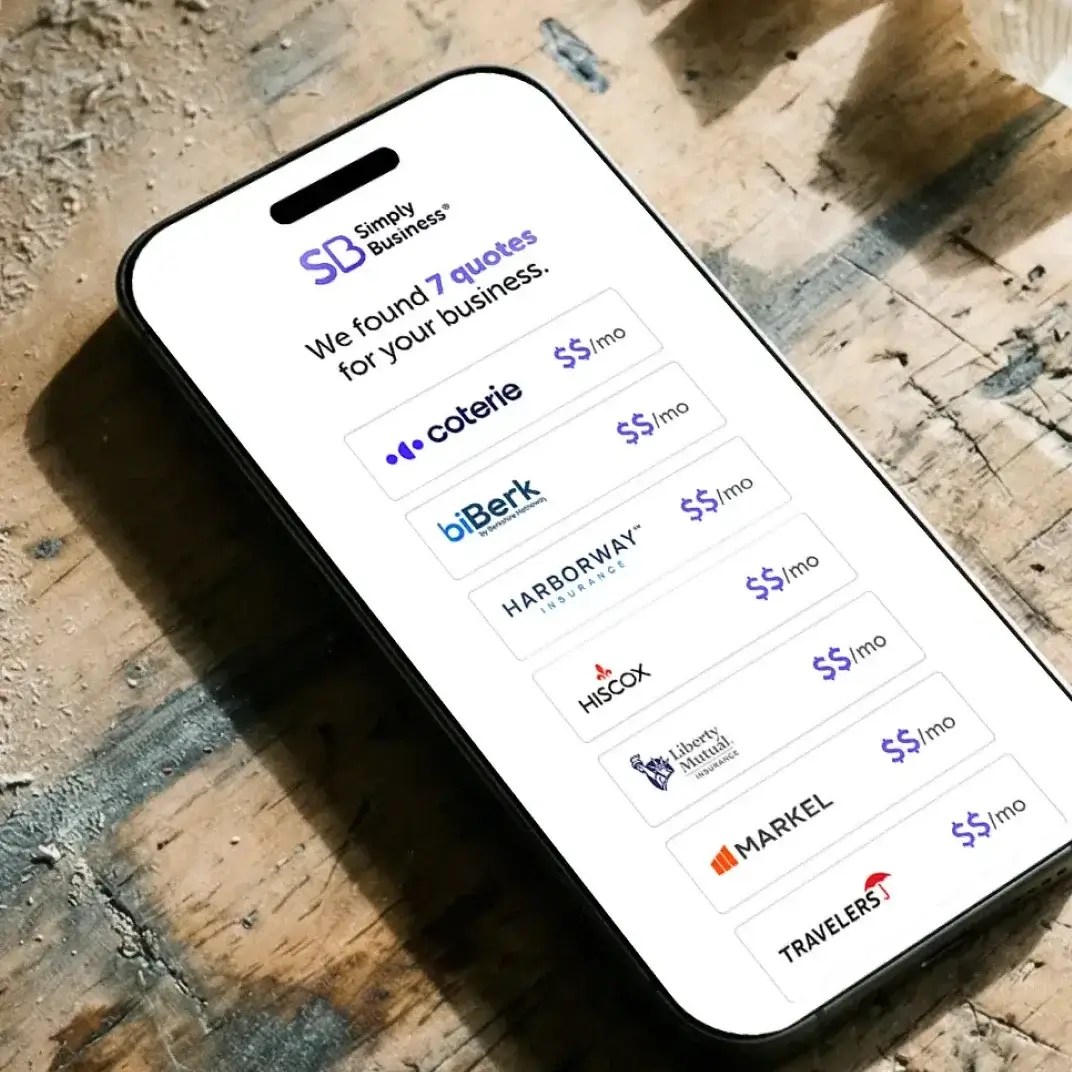

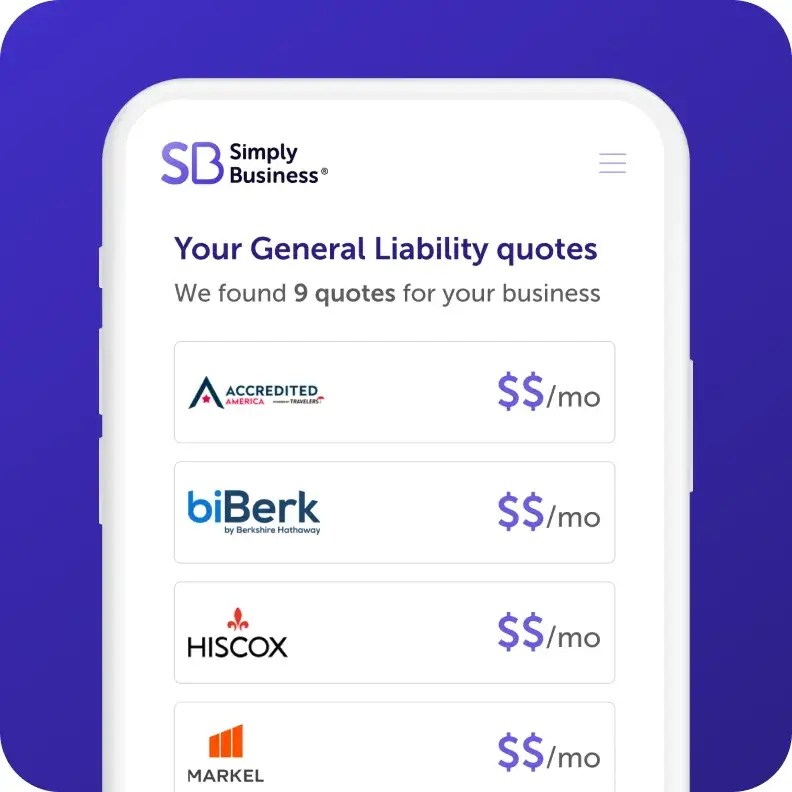

How to Get BOP Insurance Online

Start your quote

Answer a few questions about your business in one form.

Review quotes

Compare quotes side by side from top-rated insurers and customize your coverage.

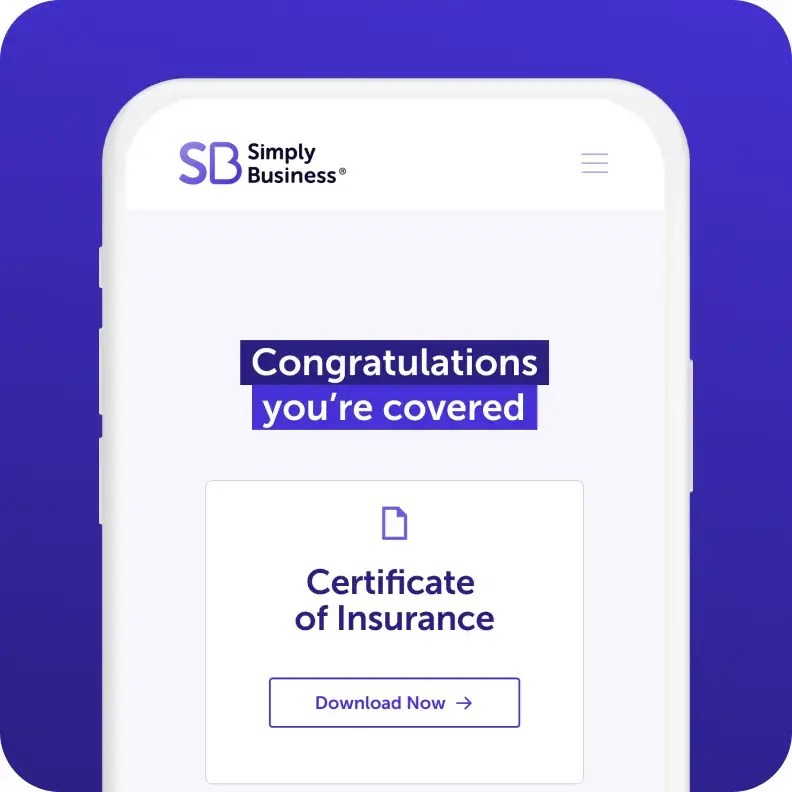

Get protected in minutes

Choose your policy, and get instant proof of insurance – all online, and all within 10 minutes.

What Is a Business Owner’s Policy (BOP)?

A one-minute explanation

Find out what a BOP covers, why you might need it, and how we can help – All in just 60 seconds.

Business Owner’s Policy FAQs

State Business Insurance Guides

Find out what’s required in the state or states where you operate:

Written by

How to Get a BOP Insurance Quote

You can quotes for general liability coverage in just 10 minutes with our online quote tool.

*Displayed price is an estimate based on the 10th percentile of business owner’s policies sold by Simply Business between January – June 2025, divided evenly across a 12 month policy term. Actual price and payment terms, including an initial down payment, may vary based on your state, insurance provider, and business.