Professional Liability Insurance (E&O) for Small Businesses

When your business relies on expertise and advice, client expectations are high — and so are the risks. Get coverage to protect your reputation, your finances, and your peace of mind for as little as $25.83/month*.

Over 1 million customers worldwide.

Buy instantly online.

Written by

What Is Professional Liability Insurance?

Professional liability insurance protects you when a client says your work caused them some sort of harm, financial or equitable. We’re talking about advice, services, or deliverables that didn’t meet expectations, or cause client harm.

You also might hear it named Errors and Omissions (E&O) insurance. It’s the same thing: coverage for claims that you made a mistake, missed something important, or didn’t deliver what was promised.

This coverage is built for service-based businesses. If your work involves expertise, judgment, or recommendations, it’s worth understanding.

Simply Business gives you access to top insurance carriers.

What Does Professional Liability Insurance Cover?

Professional liability focuses on claims tied to your work — not accidents or injuries. Here’s how it typically protects you:

Errors and Omissions

Protection against mistakes in your work

If a client claims you made an error — or left something out — E&O coverage can step in. For example, a consultant gives flawed advice that leads to lost revenue.

Even if the claim isn’t valid or is questionable, you still need to respond. That’s where E&O coverage matters.

Negligence

Defense against claims of failing to meet professional standards

Negligence claims center on expectations. A client may argue that your work didn’t meet industry standards, timelines, or the agreed-upon scope and, as a result, the client suffered damages.

This can include missed deadlines, incomplete work, or poor outcomes. E&O insurance helps you handle the fallout.

Legal Defense Costs

Coverage for lawyer fees and court settlements

Legal costs can add up quickly — even for small claims. Professional liability insurance helps cover:

- Attorney and legal fees

- Court costs

- Settlements or judgments

It’s not just about winning or losing, it’s about having the support to respond properly.

Professional Liability vs. General Liability: What’s the Difference?

Professional liability insurance

You recommend a strategy that doesn’t deliver results — the client claims financial loss. Even if your advice was reasonable, disputes can happen.

General liability insurance

A system failure, data issue, or missed deadline could disrupt a client’s operations, resulting in lost revenue and profits. That can turn quickly into a claim.

These two policies protect different risks, and many businesses need both.

Note that for most professional liability policies, legal costs and fees may impact your policy limits. Talk with your broker or agent if you have questions.

Here’s a simple way to think about it:

- Advice or service issue? Professional liability

- Physical accident? General liability

They work together, not as replacements for each other.

Who Needs Professional Liability Insurance?

If you provide expertise or services, there’s a good chance you need this coverage. Claims don’t just happen to large firms — small businesses often have negligence or malpractice claims brought against them, as well.

Here are a few common examples:

Consultants

You recommend a strategy that doesn’t deliver results — the client claims financial loss. Even if your advice was reasonable, disputes can happen.

IT professionals

A system failure, data issue, or missed deadline could disrupt a client’s operations, resulting in lost revenue and profits. That can turn quickly into a claim.

Real estate agents

An overlooked detail in your client’s home listing leads to a significantly lower sale price than your client expected or anticipated.

We can help find an E&O policy for many different types of businesses, including these:

How Much Does Professional Liability Insurance Cost?

Professional liability coverage starts at $25.83/mo., based on Simply Business customers that purchased policies between July 1, 2025 and December 31, 2025.

A few factors that influence your premium:

- Claims history

- Your profession and risk level

- Coverage limits and excess

- Business size and revenue

What Some Customers are Paying for Professional Liability2

North Carolina

Esthetician

- Limited Liability Company (LLC)

- Occurrence limit: $1M

- Deductible: $500

- Quoted May 2026

$45

/month

Pennsylvania

Business consultant

- Sole proprietorship

- Occurrence limit: $500k

- Deductible: $1,000

- Quoted May 2026

$80

/month

Florida

Bookkeeper

- Sole proprietorship

- Occurrence limit: $100k

- Deductible: $0

- Quoted May 2026

$25

/month

2These examples are real insurance quotes generated on the dates above. They are for illustration purposes only. Your coverage options and pricing may differ based on the information you provide us about your particular business, the state you operate in, the number of employees, and other factors.

What Other Types of Insurance Do I Need?

Business insurance usually refers to one or more coverages suited to your type of small business. Here are the foundational insurance policies we most often recommend, and how they can help protect your small business:

General LiabilityFrom $20.75/month*

Workers’ CompFrom $38.91/month*

Business Owner’s Policy From $33.75/month*

Inland MarineFrom $20.83/month*

Business Personal PropertyFrom $25.83/month*

Errors & OmissionsFrom $33.75/month*

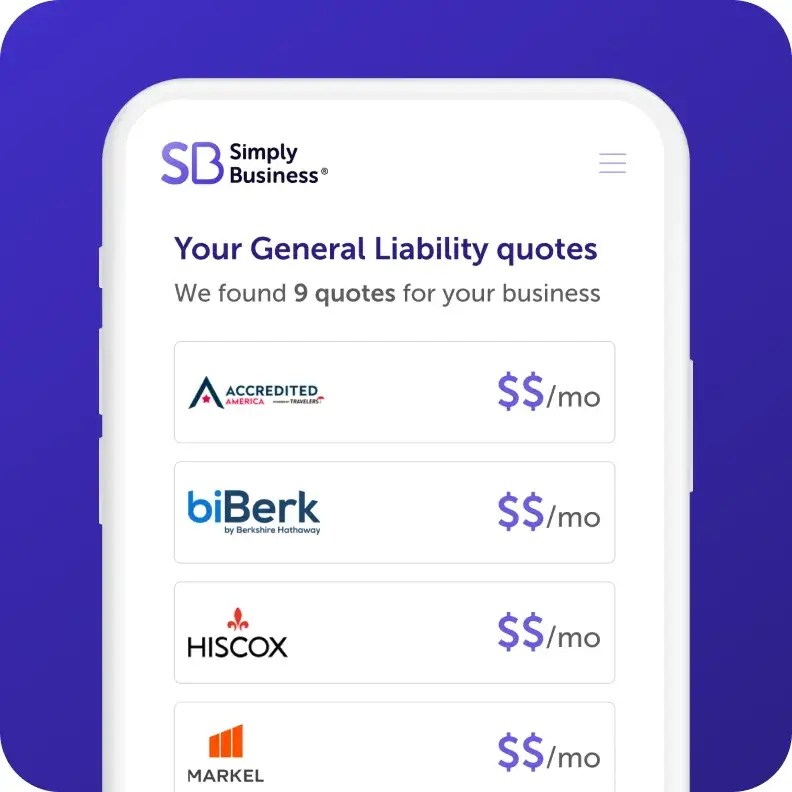

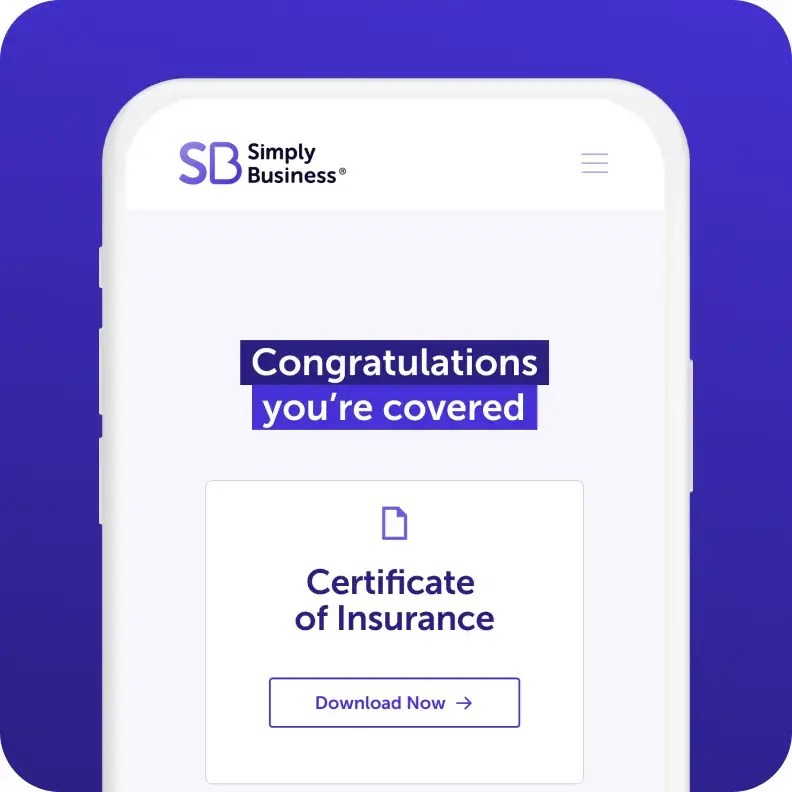

How to Get Professional Liability Insurance Online

Start your quote

Answer a few questions about your business in one form.

Review quotes

Compare quotes side by side from top-rated insurers and customize your coverage.

Get protected in minutes

Choose your policy, and get instant proof of insurance – all online, and all within 10 minutes.

Answers to More Professional Liability Insurance Questions

State Business Insurance Guides

Find out what’s required in the state or states where you operate:

Written by

How to Get a Professional Liability Insurance Quote

You can quotes for professional liability coverage in just 10 minutes with our online quote tool.

*The displayed price for each product is a monthly estimate calculated from the 10th percentile of relevant policies sold by Simply Business (e.g., General Liability data is used for General Liability estimates). This estimate uses data from relevant policy sales between July–December 2025. Final price and payment terms, which may include an initial down payment, are subject to change based on your state, selected insurance provider, and specific business details.