General Liability Insurance for Small Businesses

A cornerstone coverage to financially protect your business and provide peace of mind. Get insured for as low as $20.75/month.*

Over 1 million customers worldwide.

Buy instantly online.

Written by

What Does General Liability Insurance Cover?

General liability (GL) insurance for small businesses can help cover the costs of claims, medical bills, legal expenses, and more — which can run into tens of thousands of dollars.

If you interact with clients in any way, we typically recommend having a general liability insurance policy. This business insurance also can typically help cover your employee or employees if they cause damage. However, it doesn’t cover injuries to your employees.

Third-party property damage

General liability policies can help cover expenses if you accidentally break, damage, or destroy a client’s personal property, though it typically excludes items that are in your care, custody, or control.

Third-party injuries

If a customer is injured at your office, worksite, or in the course of your normal business operations, a general liability insurance policy can help cover their medical expenses.

Personal & advertising injury

A GL policy can help cover claims and legal expenses if you’re sued as a result of your business’s advertising, marketing, or social media activities.

Legal defense cost

General liability can cover legal defense costs for covered claims, including attorney’s fees, court costs, witness fees, and settlements or judgments up to policy limits.

What’s Not Covered by General Liability Insurance?

A general liability policy won’t help with these occurrences:

- Damage to your own property

- Damage to a customer’s personal property stored in your care, custody, and control

- Professional services

- Workers’ compensation or injury to your employees

- Damage to your work

- Auto liability

- Expected or intentional injury or damage

What Is General Liability Insurance Coverage?

Business insurance —

a one-minute explanation

Find out what GL covers, why you might need it, and how we can help — all in just 60 seconds.

Who Needs General Liability Insurance?

Sole proprietors, partnerships, LLCs, and more. General liability is a coverage we recommend for just about any business.

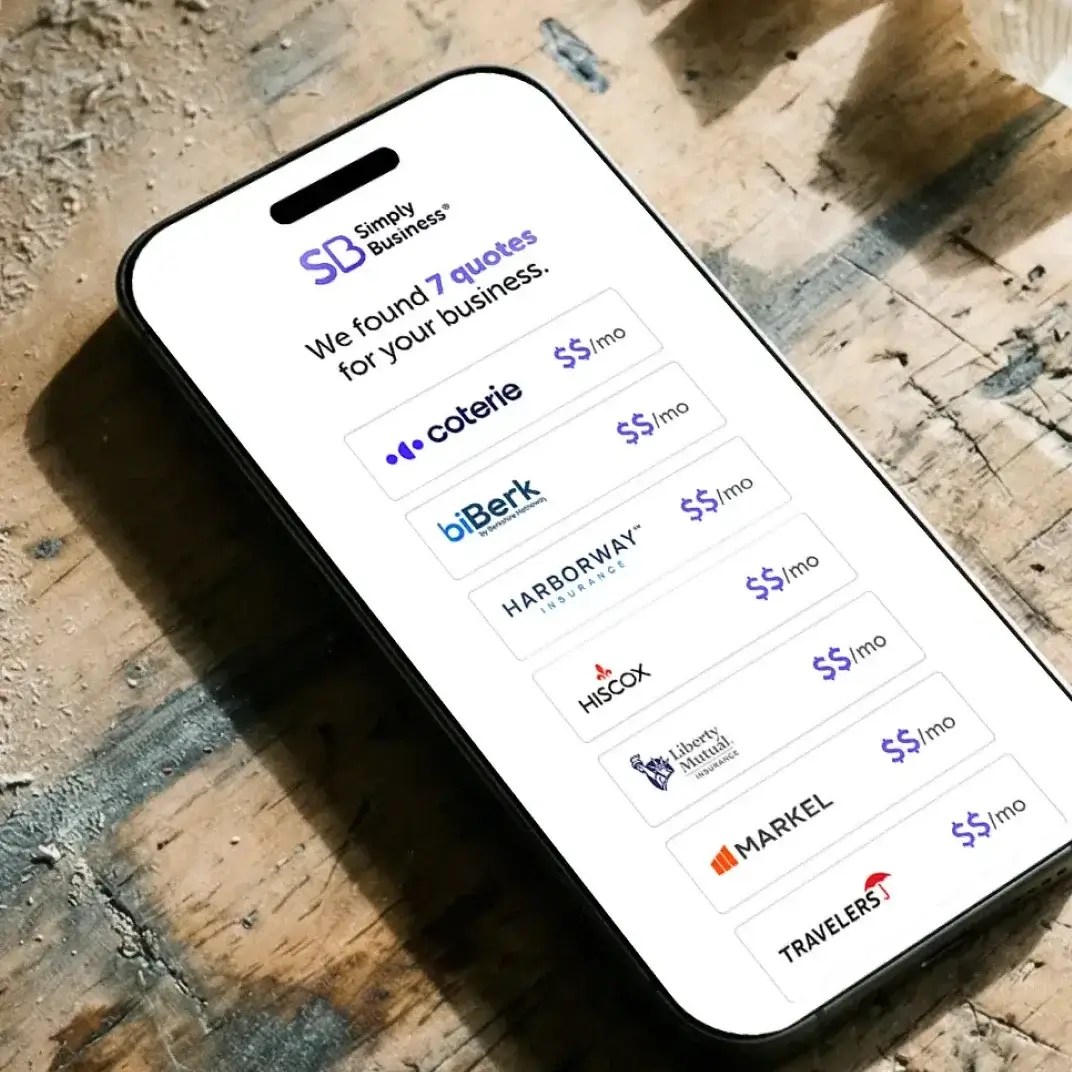

How Much is General Liability Insurance?

Compare prices from top carriers in under ten minutes.

What Some Customers are Paying for General Liability2

California

Electrician

- Limited Liability Company (LLC)

- Occurrence limit: $1M

- Aggregate limit: $2M

- Deductible: $0

- Quoted May 2026

$67/month

Texas

Lawn care services

- Sole proprietorship

- Occurrence limit: $1M

- Aggregate limit: $2M

- Deductible: $0

- Quoted May 2026

$47/month

Ohio

Handyperson

- Limited Liability Company (LLC)

- Occurrence limit: $1M

- Aggregate limit: $2M

- Deductible: $0

- Quoted May 2026

$116/month

2These examples are real insurance quotes generated on the dates above. They are for illustration purposes only. Your coverage options and pricing may differ based on the information you provide us about your particular business, the state you operate in, the number of employees, and other factors.

What Our Customers Say

This block is configured using JavaScript. A preview is not available in the editor.

General Liability FAQs

What’s the difference between general liability and professional liability insurance?

General liability insurance generally offers financial protection from claims involving third-party property damage and injuries (e.g., to customers), as well as accidents.

Professional liability insurance can often cover claims involving unintentional negligence or mistakes that you or an employee may have made while performing your work.

Learn more about the differences between general liability and professional liability.

What factors affect the cost of a general liability insurance quote?

General liability cost is largely determined by the type of work you do, the types of risks you’re exposed to, and the amount of coverage you choose.

Some other factors can include where your business is located, how many years of experience you have, and your annual revenue.

We can help find the coverages and prices for your business in just 10 minutes.

Is general liability insurance tax-deductible?

General liability insurance is usually tax-deductible since the IRS considers your policy payments to be a business expense. Keep track of all the payments you make for your policy, which will be important when you file your taxes early next year.

Keep in mind that you should always seek out the advice of an accountant or tax professional when filing your business taxes. That will make it certain your general liability policy payments will be counted as deductibles.

How do I file a claim under general liability insurance?

To file an insurance claim, contact your insurance company as soon as possible, and have the following items ready:

- Date, time, and location of the incident; brief description; parties involved.

- Photos or videos, receipts, and correspondence.

- Any formal documentation of the incident.

This could include police reports, estimated damages, proof of loss and value, or medical cost.

Is general liability insurance necessary for home-based businesses?

We recommend general liability insurance for home-based businesses, as standard homeowners’ or renters’ policies typically won’t cover business-related liabilities.

Will my policy still cover me if my business grows?

As your business grows, your current policy may not automatically cover new risks, making it crucial for you to update your coverage. Growth factors like hiring employees, buying equipment, or expanding services often require updating your policy to ensure you remain fully protected.

Why Work With Simply Business

Small business insurance is what we do. Whether it’s covering you for accidents and mistakes, meeting workers’ comp requirements, or protecting your tools and equipment, we can help find the coverage you need for your carpenter business.

We provide customized coverage options and quotes from top-rated small business insurers — all in just 10 minutes. More than 1 million small business owners worldwide trust us with their insurance, and we consistently earn high customer ratings and reviews.

We have more general liability FAQs here.

Written by

How to Get a General Liability Insurance Quote

You can quotes for general liability coverage in just 10 minutes with our online quote tool.

Feel confident in your choice.

We partner with a range of top-rated carriers and use smart technology to match you with policies that fit your specific business, your risks, and budget.

400+

business types covered

4.6/5

customer rating on Trustpilot

1M+

customers worldwide

18

top-rated small business

insurance providers

More Helpful Information About Commercial General Liability Insurance

*The displayed price for each product is a monthly estimate calculated from the 10th percentile of relevant policies sold by Simply Business (e.g., General Liability data is used for General Liability estimates). This estimate uses data from relevant policy sales between July–December 2025. Final price and payment terms, which may include an initial down payment, are subject to change based on your state, selected insurance provider, and specific business details.