Errors and Omissions (E&O) Insurance for Professionals

Insurance coverage for the costs of legal claims or damage caused by errors or unintentional omissions from your work. Get coverage for as low as $25.83/month*.

Over 1 million customers worldwide.

Buy instantly online.

What Is Errors and Omissions Insurance?

Errors and omissions (E&O) insurance, also known as professional liability, is coverage for honest mistakes. A typo in a contract. A missed deadline. An unhappy client, even when the work was solid. E&O insurance can help cover the legal costs and damages when moments like these turn into claims, so a single bad outcome doesn’t put your whole business at risk.

What Does an E&O Policy Cover?

E&O insurance covers a variety of claims that typically involve human error. That can mean errors in the work itself, claims tied to an employee’s actions, or legal disputes that arise even when you think you’ve done nothing wrong.

Negligence or alleged negligence

Errors and omissions insurance can help cover the legal costs related to claims of mistakes, poor service, or a lack of proper care.

Poor performance or results

If your business doesn’t deliver work as promised, or even if the results aren’t what your client thought or hoped they would be, a customer could sue you to recover any losses they experienced as a result. Errors and omissions insurance can help cover qualifying damages and associated legal costs.

Employees representing your business

Your E&O insurance policy can also help cover claims related to mistakes or negligence by your employees. If you have independent contractors providing services to your clients on your behalf, your E&O policy will typically cover your damages and legal fees that result from an independent contractor’s mistakes, but typically your E&O policy will not help cover the independent contractor’s own legal fees and costs. That usually requires a specific policy endorsement.

Legal defense costs

Even if you’ve done nothing wrong, a client could still sue you. Your business E&O insurance could help cover the legal costs to defend you and your business.

What Does an E&O Policy Not Cover?

No insurance policy covers every situation, and E&O is no exception. A standard policy generally generally won’t help with:

- Intentional mistakes and omissions

- Property damage

- Medical expenses

- Bodily injury

- Employee injuries

Who Needs E&O Insurance?

We recommend errors and omissions insurance for nearly any small business that provides professional services or advice. Here are some situations where an E&O policy can help different types of businesses.

Business Consultants

A client follows your strategic recommendations and loses a major account. They argue your advice was flawed causing them to lose money, and want to recover damages.

Real Estate Agents/Brokers

Your buyer closes on a home, then discovers a foundation issue. They claim you should have flagged it before closing and they’re suing you for the cost of repairs.

Insurance Agents

A small business owner files a claim, only to learn a key risk wasn’t covered. They sue you, alleging you recommended the wrong policy.

Tax Preparers

A miscategorized expense leads to an IRS penalty for your client. They say the error cost them thousands and they want you to make it right.

We can help find an E&O policy for many different types of businesses, including these:

How Much Does E&O Insurance Cost?

E&O insurance can start around $25 per month*, but your actual cost depends on the type of work you do, where you’re located, whether you have employees, the size of your payroll, the coverage you choose, and other factors.

What Some Customers are Paying for E&O Insurance2

North Carolina

Esthetician

$45/month

- Limited Liability Company (LLC)

- Limit: $1M

- Deductible: $500

- Quoted May 2026

Pennsylvania

Business consultant

$80/month

- Sole proprietorship

- Limit: $500,000

- Deductible: $1,000

- Quoted May 2026

Florida

Bookkeeper

$25/month

- Sole proprietorship

- Limit: $100,000

- Deductible: $0

- Quoted May 2026

2These examples are real insurance quotes generated on the dates above. They are for illustration purposes only. Your coverage options and pricing may differ based on the information you provide us about your particular business, the state you operate in, the number of employees, and other factors.

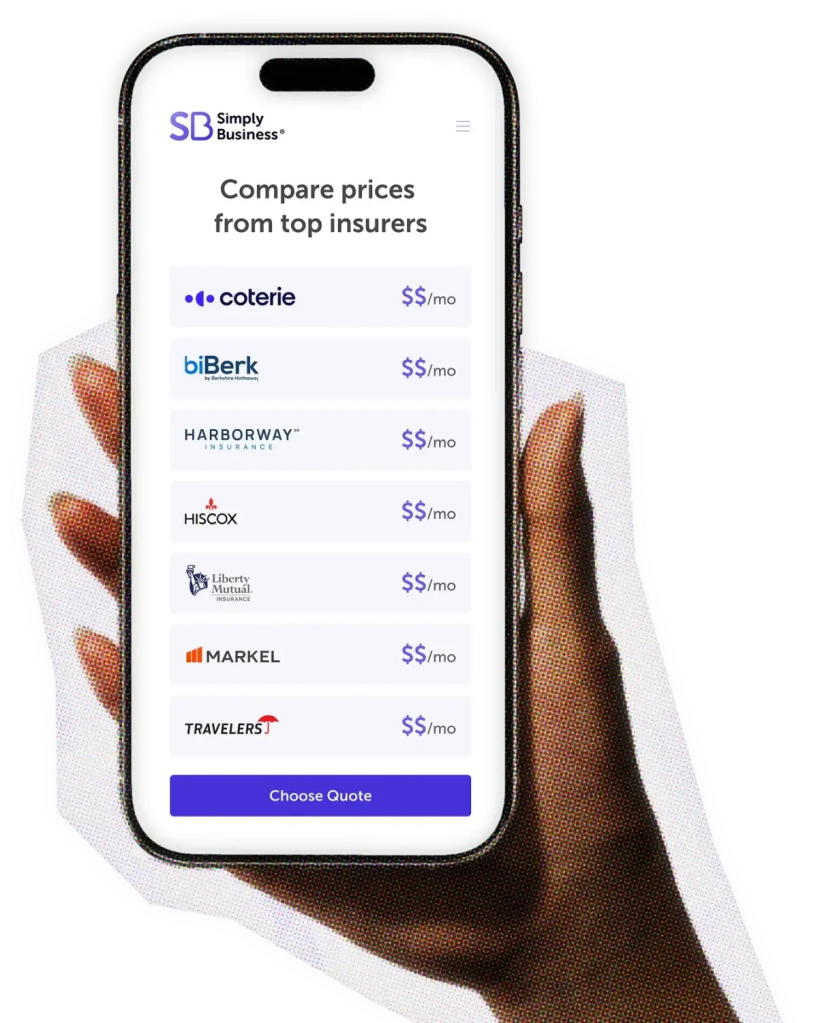

Why Choose Simply Business for Your E&O Policy?

We focus on giving you control — not complexity.

With Simply Business, you can compare quotes from multiple insurers in just minutes. That means more choice, clearer pricing, and policies that fit how you actually work.

We also keep things simple:

- Fast, easy online quotes and policy management

- Flexible coverage options

- Support when you need it

It’s about helping you feel confident in your coverage — without slowing you down.

Errors and Omissions Insurance — a one-minute explanation

Find out what E&O covers, why you might need it, and how we can help—all in just 60 seconds.

Answers to More Questions About Errors & Omissions Insurance

What does errors and omissions insurance typically cover?

Errors and omissions insurance typically covers legal defense costs, ordered damages, and settlement payouts if a client sues your business for professional mistakes. Most policies provide protection for:

- Work mistakes and oversights

- Undelivered or unfinished work

- Legal defense costs

- Missed deadlines

- Negligence

- Certain breaches of contract

Is errors and omissions insurance the same as professional liability insurance?

Generally, no—most states don’t legally require professionals to carry E&O insurance. However, certain professional licensing boards may require it to maintain your credentials and some clients may ask you to show proof of coverage before signing a contract.

Can I get a Certificate of Insurance (COI) immediately?

COIs for most insurance policies are available as soon as you purchase your policy. Once available, Simply Business provides instant digital certificate of insurance access through your online account any time of day. So if a client needs proof of E&O coverage before signing a contract, you can pull your COI and send it over in minutes.

What is the difference between E&O insurance and general liability insurance?

General liability insurance typically covers physical risks, such as third-party bodily injury or property damage. E&O insurance covers professional risks—specifically the financial losses a client might suffer due to a mistake, omission, or failure to deliver your professional services.

Does E&O insurance cover me for breach of contract?

It may help cover claims related to a breach of contract, provided the breach results directly from professional mistakes, oversight, or negligence.

What is the difference between “claims-made” and “occurrence” coverage?

E&O is typically a “claims-made” policy, meaning the policy must be active both when the alleged mistake happens and when the claim is filed. An “occurrence” policy covers any incident that occurred during your policy period, even if the claim is reported after the policy has ended. To ensure your past work remains protected, look for your policy’s retroactive date, which marks the earliest point in time an incident can occur and still be eligible for coverage.

What determines the cost of errors and omissions insurance?

The cost for your insurance coverage is usually determined by factors such as:

- The type of work you do

- Where your business is located

- Your annual revenue

- The types of policies and limits you choose

Other factors can include your claims history and how long you’ve been in business.

What should I consider before buying errors and omissions insurance?

If you’re thinking of buying errors and omissions insurance, we recommend having the following information on hand when using our errors and omissions insurance calculator:

- The state where you do business

- Your type of business or trade

- Your annual revenue estimates

This information can make it easier to get a quote from one of our insurers.

How to Get an Errors & Omissions Insurance Quote

You can quotes for errors & omissions coverage in just 10 minutes with our online quote tool.

Our +1 million customers are big fans. And you will be too.

I went online, looked around, and found Simply Business. The process was so seamless. I got my certificate within minutes. It was just phenomenal.

Karen

Owner of Tangaza Bath & Body Studio LLC

With Simply Business I know I can look at different carriers, but also see all my stuff in the same place… a lot of [insurance] providers don’t offer a variety of coverage, all in one place.

Jef

Owner of Bunker83 LLC

It wasn’t overwhelming to figure out what was covered and what wasn’t covered. And the cost was competitive.

Kim

Owner of Room to Breathe Professional Organizing

Feel confident in your choice.

We partner with a range of top-rated carriers and use smart technology to match you with policies that fit your specific business, your risks, and budget.

400+

business types covered

4.6/5

customer rating on Trustpilot

1M+

customers worldwide

18

top-rated small business

insurance providers

More Helpful Information for Small Business Professionals

*The displayed price for each product is a monthly estimate calculated from the 10th percentile of relevant policies sold by Simply Business (e.g., General Liability data is used for General Liability estimates). This estimate uses data from relevant policy sales between January–June 2025. Final price and payment terms, which may include an initial down payment, are subject to change based on your state, selected insurance provider, and specific business details.