Handyman insurance built for you

Handyman insurance built for you

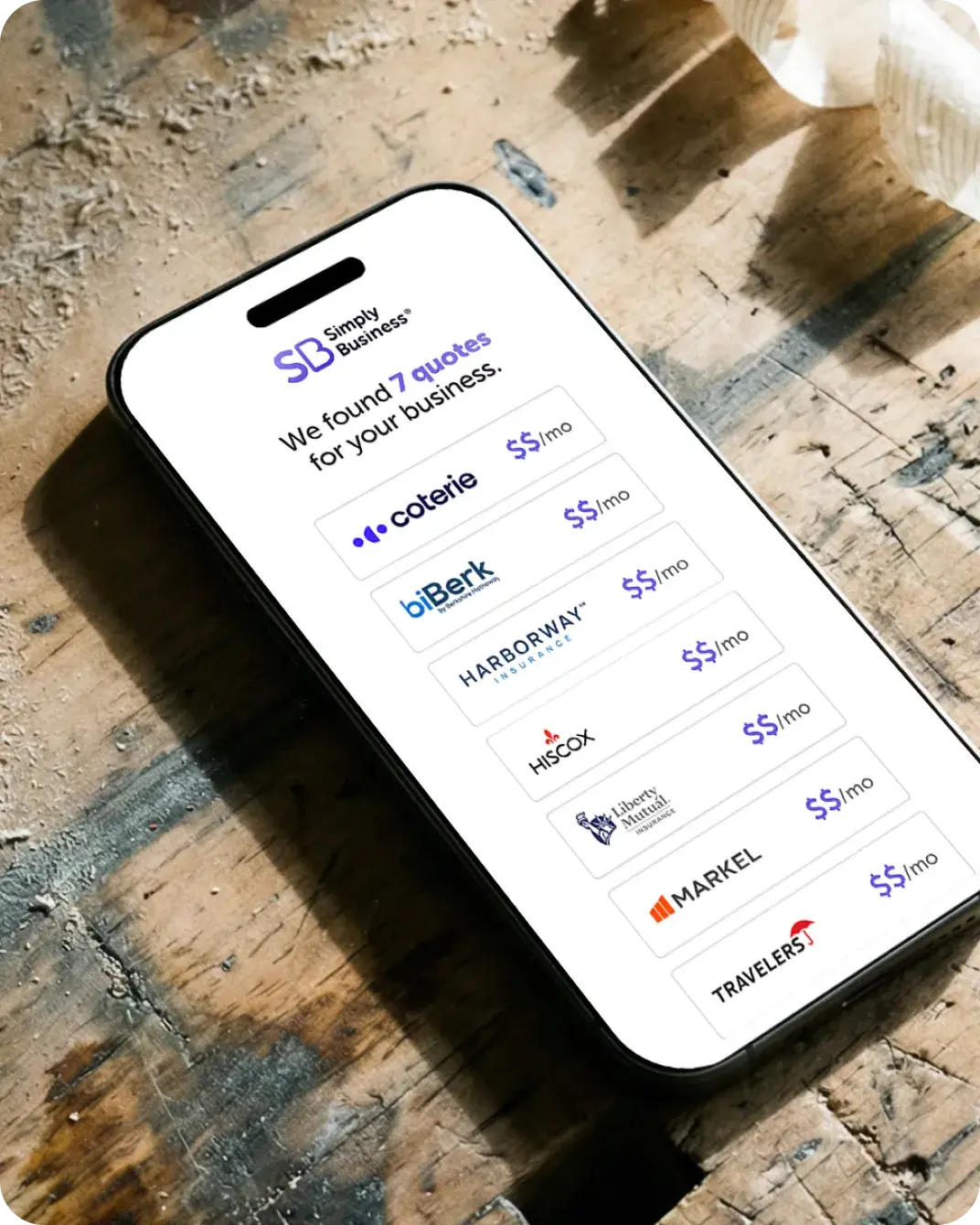

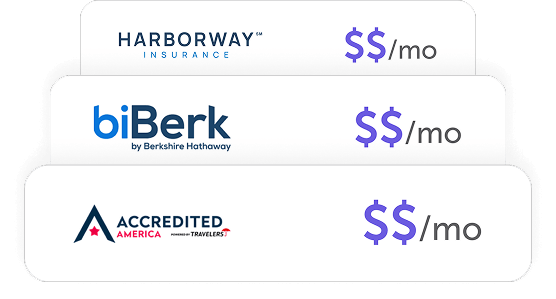

One application, multiple quotes.

All in one place.

Essential Protection

From

$41.67

/month*

Can help cover claims of accidental damage to a customer’s property, such as dents to walls or floors.

What’s included:

General Liability

Coverage limits: $1M to $2M†

Get multiple quotes in less than 10 mins

Essential Protection

From

$41.67

/month*

Can help cover claims of accidental damage to a customer’s property, such as dents to walls or floors.

What’s included:

General Liability

Coverage limits: $1M to $2M†

Get multiple quotes in less than 10 mins

Would you rather pick and choose your coverage? Explore all options

Over 1 million customers worldwide.

Buy instantly online.

Why Does a Handyman Need Business Insurance?

From patching drywall and hanging light fixtures to assembling furniture, handyman work is all about variety and precision. Whether you’re a solo fix-it pro or managing a small crew, a single slip of a drill or a stolen toolbox can disrupt your entire schedule. Handyman insurance is designed to protect your specialized tools, your business, and your team, ensuring that a minor mishap on a service call doesn’t derail your hard-earned reputation.

Below are some of the most common types of insurance policies that handyman businesses buy.

What Type of Handyman Business Insurance Do I Need?

General Liability Insurance

From

$41.67

/month*

A foundational insurance coverage to help handle costs from third-party accidents, property damage, and bodily injury.

Contractor’s Equipment and Small Tools Insurance

From

$20.83

/month†

Also known as inland marine insurance, this coverage can financially protect equipment and inventory that’s in transport or stored offsite.

Workers’ Comp Insurance

From

$38.91

/month‡

Coverage to help take care of employees who get sick or injured on the job. Most states require this coverage for small businesses with full- or part-time employees. It also can benefit business owners who don’t have employees.

Business Owner’s Policy (BOP)

From

$33.75

/month*

General liability, property insurance, and more all in one convenient package.

Business insurance —

a one-minute explanation

Learn more about policies for small businesses, what they cover, why you might need them, and how we can help – all in just 60 seconds.

What Does Handyman Insurance Cover?

When you’re juggling several service calls on a tight deadline, even a small oversight can become a major setback. Our policies help protect your handyman business and crew from these common risks:

Damage to someone else’s property

While mounting a heavy shelving unit, you accidentally strike a hidden electrical line, causing a short circuit that damages the client’s appliances. General liability insurance for a handyman could help cover the cost to repair or replace the client’s damaged equipment and protect you from other third-party damage claims.

Protection for your business property

A fire at your workshop destroys your specialized power tools and inventory, forcing you to cancel upcoming service calls. A Business Owner’s Policy (BOP) bundles general liability, commercial property protection, and business interruption coverage and can help pay for damages, repairs, and lost income so you can get back to work quickly.

Many handyman businesses choose a BOP because it offers more protection than a stand-alone general liability policy without costing much more — a great option if you’re established or planning to grow.

Care for sick or injured employees

A crew member loses their footing while descending a ladder with a toolbox and suffers a fractured ankle. Workers’ compensation insurance can help cover medical bills and provide wage replacement as your crew member recovers.

Workers’ comp is often legally required and can protect your business from costly claims, as well as taking care of your crew if they get sick or injured on the job. Even if you operate solo, we recommend workers’ comp insurance, because many health insurance policies won’t cover work-related injuries.

Damaged or stolen equipment

You arrive at a jobsite and realize your truck door was pried open and your toolbox and cordless combo kits were stolen overnight. Contractors tools and equipment insurance, also known as inland marine insurance, can help pay to replace or repair your stolen or damaged equipment, whether it’s on the move or at a jobsite.

How Much Does Handyman Insurance Cost?

Try Our Handyman Insurance Calculator

Get a quick estimate in just 3 steps.

Why Handymen Choose Simply Business

Small business insurance is what we do. Whether it’s covering you for accidents and errors, meeting workers’ comp requirements, or financially protecting your business from the unexpected, we can help find coverage for your handyman business.

Speed and Efficiency

Get customized quotes from top-rated insurers in just 10 minutes.

Tailored Coverage

Access flexible insurance options specifically built for your unique business needs.

Trusted Worldwide

Join over 1 million small business owners who rely on our highly-rated service.

Handyman Insurance FAQs

What is handyman business insurance?

Handyman insurance is a collection of policies that handyman business owners typically purchase.

Is a handyman required to have insurance by law?

Most states require that you carry workers’ compensation insurance if you have employees. There also may be licensing requirements that require certain liability coverages. And some states, such as California and Oregon, have very specific bond or liability limit requirements for handymen to maintain “exempt” status from full contractor licensing. We recommend checking with your state and local governments regarding the handyman insurance requirements you must satisfy.

Is workers’ comp required for solo handymen?

Even if you don’t have employees, many homeowners, property managers, and commercial clients require solo handymen to carry their own workers’ comp policy before starting a project. This protects them from being held liable if you’re injured on their property. Additionally, because many personal health insurance policies exclude work-related injuries, a solo policy can help cover your medical bills if you get hurt while on a service call.

Can I get a Certificate of Insurance (COI) immediately?

Once your COI is available, you can access, download, or email your Certificate of Insurance (COI) 24/7 through your Simply Business online account. Whether a homeowner asks to see your COI before you start drywall repairs or you need to provide proof to a property manager for a furniture assembly job, your digital COI should always be available in your mobile wallet or via our online COI assistant.

What determines the cost of handyman insurance?

The cost for your insurance coverage is determined by:

- The type of work you do

- Where your business is located

- Your annual revenue

- The types of policies and limits you choose

Other factors can include your claims history and how long you’ve been in business.

What should I consider before buying handyman insurance?

If you’re thinking of buying insurance for handymen, we recommend having the following information on hand when using our handyman insurance calculator:

- The state where you do business

- Your type of business or trade

- Your annual revenue estimates

This information can make it easier to get a quote from one of our insurers.

Feel confident in your choice.

We partner with a range of top-rated carriers and use smart technology to match you with policies that fit your specific business, your risks, and budget.

400+

business types covered

4.6/5

customer rating on Trustpilot

1M+

customers worldwide

18

top-rated small business

insurance providers

More Helpful Information for a Handyman Business Owner

*The displayed price for each product is a monthly estimate calculated from the 10th percentile of relevant policies sold by Simply Business (e.g., General Liability data is used for General Liability estimates). This estimate uses data from relevant policy sales between July–December 2025. Final price and payment terms, which may include an initial down payment, are subject to change based on your state, selected insurance provider, and specific business details.

† Displayed price is based on the lowest available coverage limit for Equipment and Small Tools policies.

‡ Displayed price is based on the 10th percentile of Workers’ Compensation policies sold by Simply Business to customers in your line of work between January – June 2025, divided into a 12 month policy term.

Actual price and payment terms, including an initial down payment, may vary based on your state, insurance provider, and business.