How Much Does Workers’ Compensation Insurance (WC) Cost?

The average cost of Workers’ Compensation policies purchased by Simply Business customers is $122/mo**. Your workers’ compensation cost will depend on the type of work you do, your claims history, and payroll, among other factors.

Try our Workers’ Comp Insurance calculator. Get a quick estimate in just 3 steps. No email required.

Over 1 million customers worldwide.

Buy instantly online.

Written by

What is Workers’ Compensation (WC) Insurance?

Workers’ compensation — also called workers’ comp or WC — can help cover medical bills, rehabilitation, and lost wages if an employee suffers a work-related injury or illness. It can also help protect your business from costly workplace injury lawsuits.

Most states require workers’ comp if you have employees. Even if you operate solo, it’s worth considering — many health insurance policies don’t cover work-related injuries. Beyond the likely statutory requirements, without coverage, you could face massive out-of-pocket medical bills.

This guide breaks down what workers’ comp typically costs, what drives the price, and how to get a quote through Simply Business.

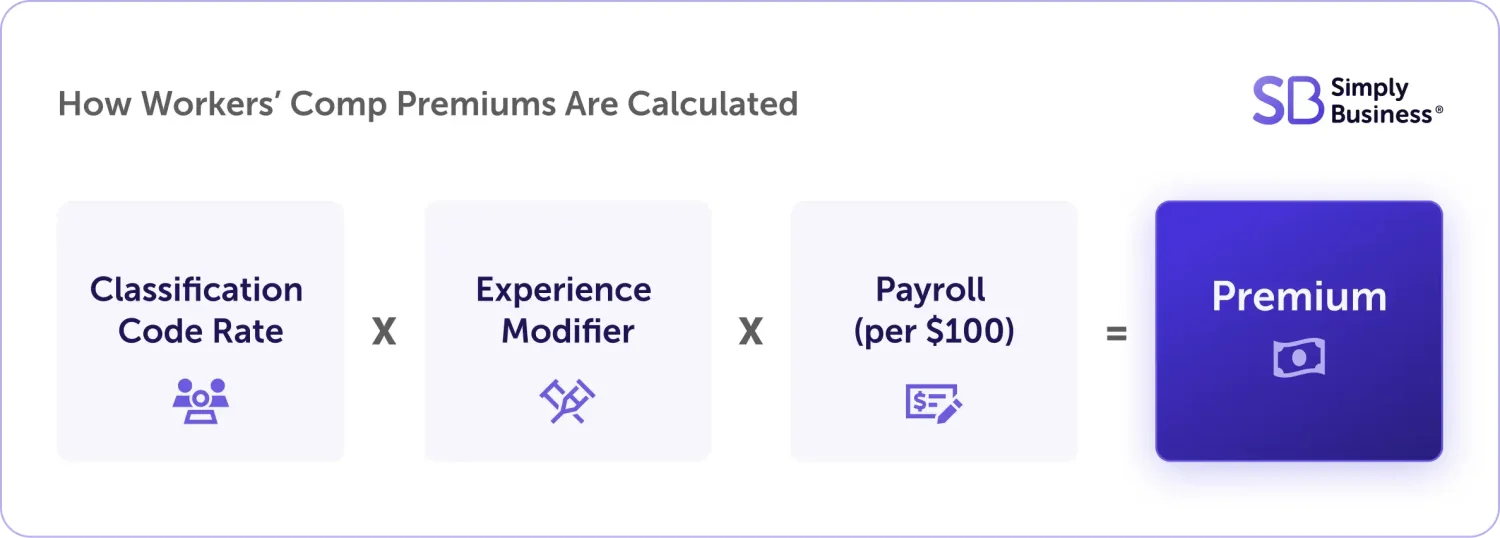

How Is Your Workers’ Compensation Insurance Cost Calculated?

Workers’ comp premiums are determined by a formula that considers your industry’s risk level, your business’ claims history, and your payroll.

Classification codes: These are assigned by insurance companies or state rating bureaus to categorize businesses by risk level, based on their industry and the nature of their work. Construction work typically has more risks than photography, so it will typically have a higher classification rate.

Experience modifier (X-Mod or EMR): This is based on the number of claims your business has had compared to other businesses with the same classification during a particular look-back period. Businesses with a workers’ comp history of less than four years typically have an X-Mod of 1.0, which is the baseline average for businesses in your classification. An X-Mod above 1.0 indicates more claims or losses than average, potentially resulting in higher premiums.

Payroll: This is what you paid to employees, including wages, salaries, and benefits. The premium is often calculated using a percentage payroll.

How the calculation works:

Let’s say you have a new HVAC business in Florida with a payroll of $75,000. The classification rate is 4.36 per $100 of payroll and your X-Mod is 1.0.

Assuming your workers’ comp carrier uses this formula, your premium calculation would be ($75,000/100) x 4.36 x 1.00 = $3,270.

What Factors Affect Your Workers’ Compensation Insurance Cost?

Several key factors affect your workers’ comp insurance cost.

Industry

Insurers use classification codes to define the risk level of your industry, so the type of work you and your employees do is a primary cost driver. A roofing company will likely have a much higher workers’ compensation rate per $100 of payroll than an accounting firm because the physical risk of injury is substantially higher.

Median Monthly Workers’ Comp Premiums by Trade/Industry

Here’s a look at the median monthly cost for workers’ compensation insurance for some of our most common trades or industries.

| Industry | Median Monthly Cost1 |

|---|---|

| Combined heating and air conditioning installation and repair (HVAC) | $139 |

| Electrical work | $108 |

| Handyperson | $157 |

| Housekeeping | $103 |

| Janitorial services | $91 |

| Landscaping services | $112 |

| Lawn care services | $100 |

| Painting and wall covering contractors | $164 |

| Plumbing | $126 |

1Data from Simply Business customers who purchased a workers’ compensation policy from July 1, 2025 to December 31, 2025. The median costs shown are for illustrative purposes only; actual premiums vary by state, coverage limits, and individual business risk.

Claims history

A clean claims history is one of the best ways to keep your workers’ comp insurance cost low. Your Experience Modification Rate (EMR) compares your claims history to the industry average — and a lower EMR can significantly reduce your workers’ comp rates.

Payroll

Workers’ comp premiums are calculated per $100 of your gross payroll — the higher your payroll, generally the higher your premium.

Location

Each state has its own workers’ comp laws and most use state or national rate-setting bureaus, so your premium can vary significantly depending on where your employees work. State costs differ based on benefit levels, medical fee schedules, and the local insurance market, with a few states requiring you to buy coverage directly from a government fund.

Median Monthly PL Premiums by State

| State | Median Monthly Cost2 |

|---|---|

| California | $108 |

| Colorado | $126 |

| Florida | $92 |

| Georgia | $123 |

| Maryland | $59 |

| Massachusetts | $113 |

| Michigan | $89 |

| New Jersey | $111 |

| North Carolina | $120 |

| Pennsylvania | $90 |

| South Carolina | $127 |

| Tennessee | $98 |

| Texas | $66 |

| Virginia | $100 |

2Data from Simply Business customers across some of our most common states, who purchased a workers’ compensation policy from July 1, 2025 to December 31, 2025. The median costs shown are for illustrative purposes only; actual premiums vary by state, coverage limits, and individual business risk.

Policy limits

Workers’ compensation benefits themselves are set by state law, but your employer’s liability limits — which cover related lawsuits — can be adjusted. Higher coverage usually means a higher premium. But it also means more protection if something goes wrong.

And don’t forget the deductible — what you pay out of pocket before insurance kicks in. In many states, employers can opt into workers’ comp deductible programs, agreeing to cover a portion of each claim in exchange for a reduced premium.

For more information, consult with a legal professional in your state or with one of our licensed agents.

How to Save on Workers’ Compensation (WC) Insurance

- Reduce your risks

Fewer claims can mean lower rates. That’s why risk management should be a top priority:

→ Learn from past claims and put steps in place to prevent future mishaps.

→ Train your team on safety procedures and best practices.

→ Keep your space safe by minimizing risks like trip hazards. - Return-to-work program

Bringing injured employees back on light or modified duty as soon as it’s safe for them to do so lowers the total cost of a claim — and lower claim costs feed directly into your EMR, which can mean lower premiums down the road. - Shop Around

Simply Business provides customized coverage options from top-rated small business insurance providers — all in just 10 minutes. We do the legwork so you can sit back, compare quotes, and save. - Pay-as-you-go

Instead of paying a large annual workers’ comp estimate, consider a pay-as-you-go billing option, which can sync directly with your payroll, improving cash flow and minimizing surprises at your WC audit.

Simply Business gives you access to top carriers:

What Some Customers are Paying for Workers’ Compensation3

Massachusetts

Electrician

$111/month

- Limited Liability Company (LLC)

- 1 employee

- Quoted May 2026

Texas

Handyperson

$137/month

- S-Corp

- 2 employees

- Quoted May 2026

Michigan

Lawn care

$95/month

- Sole Proprietorship

- 2 employees

- Quoted May 2026

3These examples are real insurance quotes generated on the dates above. They are for illustration purposes only. Your coverage options and pricing may differ based on the information you provide us about your particular business, the state you operate in, the number of employees, and other factors.

How to Get General Liability Insurance Online

Step 1: Start your quote

Answer a few questions about

your business in one form.

Step 2: Review quotes

Compare quotes side by side

from top-rated insurers and customize

your coverage.

Step 3: Get protected in minutes

Choose your policy, and in most cases, get instant proof of insurance – all online,

and all within 10 minutes.

Step 1: Start your quote

Answer a few questions about

your business in one form.

Step 2: Review quotes

Compare quotes side by side

from top-rated insurers and customize

your coverage.

Step 3: Get protected in minutes

Choose your policy, and in most cases, get instant proof of insurance – all online,

and all within 10 minutes.

Why Choose Simply Business

Small business insurance is what we do. Whether it’s covering you for accidents and errors, meeting workers’ comp requirements, or financially protecting your business from the unexpected, we can help find the coverage you need for your small business.

Speed and Efficiency

Get customized quotes from top-rated insurers in just 10 minutes.

Tailored Coverage

Access flexible insurance options specifically built for your unique business needs.

Trusted Worldwide

Join over 1 million small business owners who rely on our highly-rated service.

Workers’ Compensation FAQs

What does workers’ compensation Insurance cover?

Workers’ comp can help cover a range of costs when an employee suffers a work-related injury or illness, including:

- Medical expenses: Exams, tests, hospitalization, and surgeries.

- Rehabilitation costs: Physical therapy and ongoing care to help an injured employee recover and return to work.

- Lost wages: If an employee can’t work because of a work-related injury or illness, the employee could receive a portion of their average weekly wage, typically paid in weekly or bi-weekly installments.

- Survivor benefits: In the event of the worst, workers’ comp Insurance can help cover end-of-life expenses.

What is NOT covered by workers’ compensation insurance?

Workers’ comp generally won’t cover:

- Third-party injuries: Client, vendor, or visitor injuries — which are typically covered by general liability insurance.

- Off-the-clock injuries: Injuries or illnesses that occur outside of scope-of-employment duties.

- Impairment or misconduct: Injuries resulting directly from an employee’s intoxication, illegal drug use, or intentional willful misconduct.

- Standard commutes: Routine travel to and from work, with limited exceptions such as traveling for a dedicated business errand.

Can I get a Certificate of Insurance (COI) immediately?

Yes. COIs for most policies are available soon after you purchase your coverage. With Simply Business, you can download and share your COI instantly through your online account or right from your phone — useful when a GC, client, or licensing board asks for proof of coverage before you start a job.

What if I already have health insurance?

A standard health insurance plan may not cover a work-related illness or injury. Plus, most health insurance plans won’t cover lost income as a result of your injury.

Is workers’ comp legally required in most states?

Yes. Most states require workers’ comp once you have employees, though the rules vary widely. Some require WC coverage from the first hire, while others set thresholds — often 3 to 5 employees — before coverage kicks in. Higher-risk industries often have stricter rules and may require coverage regardless of headcount.

For the rules specific to your state and industry, consult with your state’s workers’ comp agency or one of our licensed agents.

As a 1099 hire, am I automatically covered if I’m hired by a general contractor?

Usually not. Being a 1099 independent contractor typically means you’re responsible for your own insurance, including workers’ compensation — even when you’re working on a general contractor’s (GC) job site. In fact, many GCs require their subcontractors to provide proof of their own coverage before starting a project. And without your own policy in place, a work-related injury could leave you personally responsible for medical bills and lost income.

What is a ghost policy and how does it compare to a full workers’ comp policy?

A workers’ comp ghost policy is designed for sole proprietors and independent contractors who don’t carry full coverage but still need proof of workers’ compensation insurance to meet contractual requirements, satisfy client or contractor demands, or demonstrate professionalism. It’s called a “ghost policy” because it provides documentation of insurance without insuring you or any workers. Unlike a full workers’ comp policy, a ghost policy doesn’t cover your injuries but it can be a more affordable way to satisfy hiring requirements.

What happens if I don’t have workers’ compensation Insurance?

Work-related accidents can happen, and when they do it can be costly if you don’t have workers’ comp coverage. According to the National Safety Council, the average workers’ comp claim from a workplace slip or fall now runs over $54,000. Going without required coverage can also mean steep fines and stop-work orders — it’s best to check with your state agencies for specifics.

Where can I buy a WC policy?

For most small businesses, the simplest path is through a licensed agent like Simply Business, where you can compare WC quotes from multiple carriers and find coverage that fits your state, industry, and payroll.

Four states — Ohio, Washington, North Dakota, and Wyoming — are the exception. They’re monopolistic, meaning you can’t purchase a policy from a private insurer. Coverage has to come through the state-run fund.

We have the following guides to get you started:

California, Colorado, Florida, Georgia, Illinois, Maryland, Minnesota, New Jersey, New York, North Carolina, Pennsylvania, Texas, Wisconsin.

Is workers’ comp insurance tax-deductible?

Typically yes. Premiums for your workers’ comp (WC) policy are generally considered a tax-deductible business expense. Keep records of your payments throughout the year so they’re easy to claim at tax time, and always check with your accountant or tax professional to confirm what applies to your specific business.

Written by

Our +1 million customers are big fans. And you will be too.

I went online, looked around, and found Simply Business. The process was so seamless. I got my certificate within minutes. It was just phenomenal.

Karen

Owner of Tangaza Bath & Body Studio LLC

With Simply Business I know I can look at different carriers, but also see all my stuff in the same place… a lot of [insurance] providers don’t offer a variety of coverage, all in one place.

Jef

Owner of Bunker83 LLC

It wasn’t overwhelming to figure out what was covered and what wasn’t covered. And the cost was competitive.

Kim

Owner of Room to Breathe Professional Organizing

This block is configured using JavaScript. A preview is not available in the editor.

Feel confident in your choice.

We partner with a range of top-rated carriers and use smart technology to match you with policies that fit your specific business, your risks, and budget.

400+

business types covered

4.6/5

customer rating on Trustpilot

1M+

customers worldwide

18

top-rated small business

insurance providers

More Helpful Information About Workers’ Compensation Insurance

4-minute read

The Basics of Workers’ Comp

**Median cost figure is based on the costs of policies purchased by Simply Business customers (e.g., General Liability data is used for General Liability estimates) from July 1, 2025 – December 31, 2025.